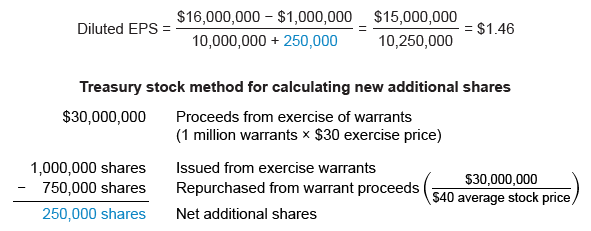

XYZ Corporation has 10 million shares of common stock outstanding and has not issued or repurchased common stock this year. Several years ago, it issued $10 million in bonds with 1,000,000 warrants attached. Each warrant allows the holder to purchase one share of XYZ common stock for $30. The average market price per share for XYZ stock this year is $40. It also paid dividends of $1 million on its nonconvertible preferred stock. If XYZ has a net income of $16 million this year, the diluted earnings per share that XYZ will report is closest to:

A warrant is essentially an option allowing the holder of the warrant the right to purchase shares of common stock at a predetermined price. Exercising a warrant causes the number of common shares outstanding to increase. This increase usually causes the company's earnings-per-share (EPS) to decrease, so warrants are dilutive securities.

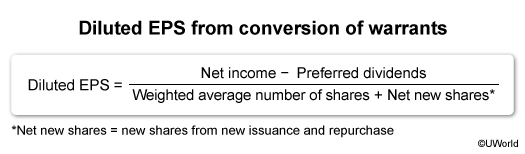

When calculating EPS, warrants are treated as having been exercised at the earlier of the beginning of the accounting period, if the warrants were then outstanding, or the date of issuance. Both IFRS and GAAP require companies to use the treasury stock method for calculating the effect of warrants on EPS. An example of XYZ's use of the treasury stock method is shown below.

A key assumption underlying the treasury stock method is that the average market price of the stock is more than the exercise price, so the proceeds will purchase fewer shares than were issued from the warrants' exercise. The resulting weighted average is then used to calculate diluted EPS. An example of XYZ's use of the treasury stock method is shown below.

(Choice A) $1.36 is obtained when the denominator is increased by the total number of shares issued from the warrants' exercise (1,000,000) instead of the net shares added (250,000).

(Choice B) $1.56 results from neglecting to subtract the preferred dividend from net income in the numerator.

Things to remember:

When warrants (or employee stock options) are part of a company's capital structure, they are treated as dilutive securities. IFRS and GAAP both require the company to use the treasury stock method for calculating diluted earnings per share.