Inflation has been a defining economic concern in recent years, with policymakers, businesses, and individuals feeling its effects. While inflation rates have declined significantly from historic highs, they still remain above the 2% target set by the Federal Reserve (Fed) and are impacting sectors unevenly. We'll explore how we got here, and what actions the government has taken to lower inflation rates and stabilize the economy.

How COVID-Era Policies Shaped Inflation Trends

When the COVID-19 pandemic began, it represented more than a major health crisis. It threatened to destabilize the global economy and put millions of people out of work. In the United States, more than 23 million jobs were initially lost, leading to a recession in early 2020.[1] Congress responded with dramatic increases in fiscal spending, while the Fed lowered interest rates to near zero and implemented aggressive quantitative easing policies. During this period, countries were locking down, as well, which drastically disrupted supply chains and labor markets. All of this together set the stage for the soaring inflation seen from mid-2021 to mid-2023, which reached a peak of 9.1% in June 2022.[2]

How the Government Responded to COVID and Increasing Inflation

The 9.1% inflation rate (calculated using the Consumer Price Index — what we will use in our analysis) in June 2022 was the highest level seen in the past 4 decades. What factors drove inflation this high, and what made this the peak instead of 12.3% like in 1974 or 14.8% in 1980[3] when the U.S. experienced stagflation?

Aggressive, Yet Consistent Monetary Policy

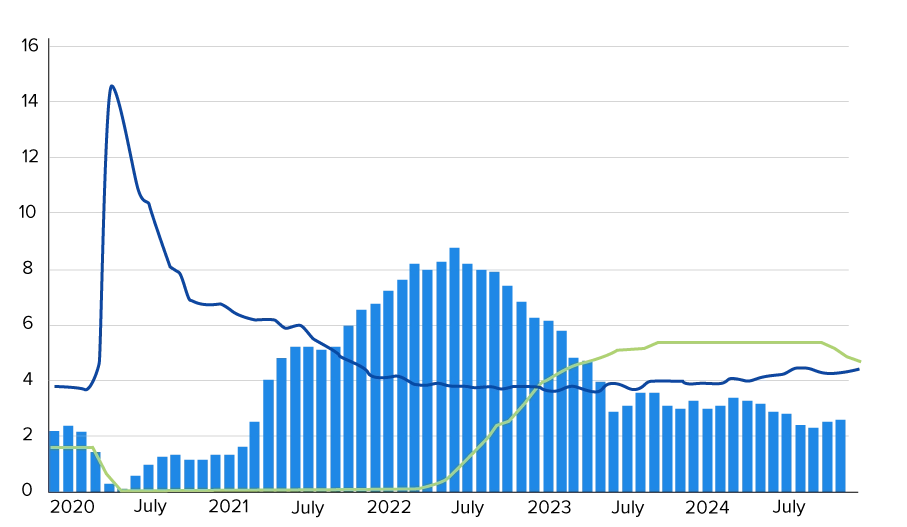

Inflation began to creep upward in early 2021 as the Fed maintained its loose monetary policy to stimulate economic growth. After steadying around 5% to 5.5% in the summer of 2021, inflation rates continued to rise. Instead of immediately raising interest rates as inflation ticked upward, the Fed kept an eye on the still high unemployment rate. As unemployment lowered to the Fed's unofficial target of 4% in late 2021, the Fed felt more comfortable tightening its monetary policy, which occurred throughout 2022.

Fig. 1: Navigating Tenuous Economic Conditions with Monetary Policy Post-COVID[3][4][5]

Concurrently, the Fed implemented aggressive quantitative easing policies by purchasing large amounts of debt securities. These policies shifted throughout the pandemic as the situation matured. Below is a timeline offered by the Brookings Institute:[6]

- On March 15, 2020, the Fed signaled it would buy at least $500 billion in Treasury securities and $200 billion in government-guaranteed mortgage-backed securities over the coming months.

- On March 23, 2020, the Fed updated its guidance to purchases "in the amounts needed to support smooth market functioning and effective transmission of monetary policy to broader financial conditions."

- In June 2020, purchases were set to at least $80 billion a month in Treasurys and $40 billion in residential and commercial mortgage-backed securities until further notice.

- In December 2020, the Fed aimed to slow purchases once the economy made "substantial further progress" toward the Fed's price stability and maximum employment goals.

- In November 2021, asset purchases were tapered by $10 billion in Treasurys and $5 billion in mortgage-backed securities each month.

- In December 2021, the pace of tapering was doubled to $20 billion in Treasurys and $10 billion in mortgage-backed securities each month.

You can take a deeper dive into the Fed's actions during COVID here. Overall, the Fed's response to the COVID pandemic has been viewed as generally positive, with concerns related to long-term effects and inflation. While monetary policy can influence the rates of inflation and unemployment by speeding up or slowing down economic growth (via money supply), it's important to note that it's only 1 piece of the puzzle.

Fiscal Policy and Deficit Spending

Four major pieces of legislation were passed during the COVID period that dramatically impacted the economy and inflation rates. These spending packages came on top of what were already some of the largest budget deficits in U.S. history, and are generally viewed with greater controversy than the Fed's actions.

Two acts were directly related to COVID relief. The Coronavirus Aid, Relief, and Economic Security (CARES) Act was signed into law in March 2020 and aimed to provide a softer economic landing in direct response to COVID. It received near-unanimous support, passing with a 419-6 vote in the House and 96-0 vote in the Senate,[7] representing lawmakers' urgency to provide support amidst the pandemic. The American Rescue Plan Act was signed into law in March 2021 and intended to provide further relief in response to the ongoing effects of COVID. It received a 219-212 vote in the House and 50-49 vote in the Senate,[8] indicating division among lawmakers over how to address lingering COVID concerns. Spending on these acts, and supplemental legislation, totaled over $4.6 trillion.[9]

In November 2021, the Infrastructure Investment and Jobs Act was signed into law. While not directly related to COVID relief, it aimed to address some of the lingering concerns from COVID by improving infrastructure, stimulating the economy, and making targeted economic investments. This act passed with a 221-201 vote in the House and 69-30 vote in the Senate.[10] It was criticized for its $1.2 trillion price tag,[11] funding mechanisms, and scope.

In August 2022, the Inflation Reduction Act was signed into law. Perhaps the most controversial of the 4, it received a 220-213 vote in the House and 51-50 vote in the Senate.[12] This act was named after reducing inflation but focused largely on investments in clean energy, manufacturing, and the climate. Hopes are that the act will reduce the deficit and inflation over time through economic growth in specific sectors, reduced healthcare costs, stricter corporate taxes, and elevated IRS funding. Whether this will occur is hotly debated. Some argue that the act's costs are greatly underestimated, while others say the fiscal costs will be offset by reduced economic costs. Either way, most agree it did not bring inflation down from 2022 highs and should be viewed as longer-term legislation.

All of this spending has had, and will continue to have, tremendous impacts on the economy and inflation rates. Budget deficits during this period were $3.13 trillion in 2020, $2.77 trillion in 2021, $1.38 trillion in 2022, $1.70 trillion in 2023, and $1.83 trillion in 2024.[13] Total national debt in 2024 was approximately $36 trillion.[14]

Navigating Persistent Challenges

When considering inflation data and the fiscal decisions made during the COVID period, it's important to recognize that different sectors of the economy were impacted unevenly. This led to a disparity in cost increases, better explains some of the government's investments, and completes the picture of where we stand today.

Energy, gasoline, and natural gas saw the highest spikes, with peak price increases of 41.6%, 59.9%, and 38.4%, respectively.[15] Much of this was due to simple supply and demand as economies ramped up following COVID. These effects were then prolonged due to geopolitical tensions and Russia's invasion of Ukraine in 2022. These spikes played a large role in the inflation highs experienced in 2022. Paired with disrupted supply chains and labor shortages, massive ripple effects were felt throughout the transportation, electronics, food, and construction industries. Additionally, sectors sensitive to interest rate increases are feeling the impact of the Fed's tightened monetary policy, such as commercial real estate and housing.

Ultimately, recovering from the economic fallout of the COVID pandemic is a journey, not a destination. The inflation rate decline since the highs experienced in 2022 represents progress, but there's still work to be done.

Lessons for CFA Candidates

The past 5 years are an excellent example of how monetary policy, fiscal policy, and global market conditions can affect the economy.

- Monetary Policy: The Fed's interest rate adjustments and quantitative easing measures illustrate the trade-offs between inflation control and economic growth.

- Fiscal Policy: Legislation passed during the COVID period shows how government spending and investment priorities can shape economic outcomes in the short and long term.

- Economic Indicators: Understanding the interplay between official metrics and real-world impacts is crucial for analyzing financial markets and economic policies.

As the Fed and policymakers continue to navigate these waters, CFA candidates can learn valuable lessons about the complex and multifaceted nature of our economy. We remain committed to supporting your CFA journey by providing detailed insights into these critical topics. Together, we can master the complexities of modern finance and economics.

—-

Disclaimer: The information provided in this blog is for informational purposes only and does not constitute financial, investment, or legal advice. The opinions expressed are those of the authors and do not necessarily reflect the views or policies of UWorld. While every effort has been made to ensure the information is accurate, it may not be up-to-date or applicable to all circumstances. Readers are encouraged to consult a qualified financial professional for advice tailored to their needs and objectives. UWorld disclaims any liability for decisions made based on this content.

References

- "What Caused the High Inflation during the COVID-19 Period?" U.S. Bureau of Labor Statistics, December 2023, www.bls.gov/opub/mlr/2023/beyond-bls/what-caused-the-high-inflation-during-the-covid-19-period.htm.

- "Consumer prices up 9.1 percent over the year ended June 2022, largest increase in 40 years." U.S. Bureau of Labor Statistics, 18 July 2022, https://www.bls.gov/opub/ted/2022/consumer-prices-up-9-1-percent-over-the-year-ended-june-2022-largest-increase-in-40-years.htm.

- "United States Inflation Rate." Trading Economics, December 2024, tradingeconomics.com/united-states/inflation-cpi.

- "Federal Funds Effective Rate." FRED Economic Data, Federal Reserve Bank of St. Louis, 2 December 2024, https://fred.stlouisfed.org/series/FEDFUNDS.

- "United States Unemployment Rate." Trading Economics, December 2024, https://tradingeconomics.com/united-states/unemployment-rate.

- "What did the Fed do in response to the COVID-19 crisis?" Brookings, The Brookings Institute, 2 January 2024, .https://www.brookings.edu/articles/fed-response-to-covid19/.

- "Actions - H.R.748 - 116th Congress (2019-2020): CARES Act." Congress.gov, Library of Congress, 27 March 2020, https://www.congress.gov/bill/116th-congress/house-bill/748/all-actions.

- "Actions - H.R.1319 - 117th Congress (2021-2022): American Rescue Plan Act of 2021." Congress.gov, Library of Congress, 11 March 2021, https://www.congress.gov/bill/117th-congress/house-bill/1319/all-actions.

- "The Federal Response to COVID-19." COVID-19 Spending, USAspending.gov, 30 September 2024, https://www.usaspending.gov/disaster/covid-19.

- "Actions - H.R.3684 - 117th Congress (2021-2022): Infrastructure Investment and Jobs Act." Congress.gov, Library of Congress, 15 November 2021, https://www.congress.gov/bill/117th-congress/house-bill/3684/all-actions.

- "Bipartisan Infrastructure Law (BIL) / Infrastructure Investment and Jobs Act (IIJA)." U.S. Department of Transportation, 16 February 2023, https://www.phmsa.dot.gov/legislative-mandates/bipartisan-infrastructure-law-bil-infrastructure-investment-and-jobs-act-iija.

- "Actions - H.R.5376 - 117th Congress (2021-2022): Inflation Reduction Act of 2022." Congress.gov, Library of Congress, 16 August 2022, https://www.congress.gov/bill/117th-congress/house-bill/5376/all-actions.

- "What is the national deficit?" FiscalData.Treasury.gov, Data Transparency, 30 September 2024, https://fiscaldata.treasury.gov/americas-finance-guide/national-deficit/.

- "What is the national debt?" FiscalData.Treasury.gov, Data Transparency, December 2024, https://fiscaldata.treasury.gov/americas-finance-guide/national-deficit/.

- "Graphics for Economic News Releases." U.S. Bureau of Labor Statistics, December 2024, https://www.bls.gov/charts/consumer-price-index/consumer-price-index-by-category-line-chart.htm.