Deferred tax items (ie, deferred tax assets and liabilities) arise from the difference between income tax expense (for accounting purposes) and taxes payable (for tax reporting) for a period. Differences can occur as tax expense is calculated according to accounting standards and taxes payable are calculated according to the tax code.

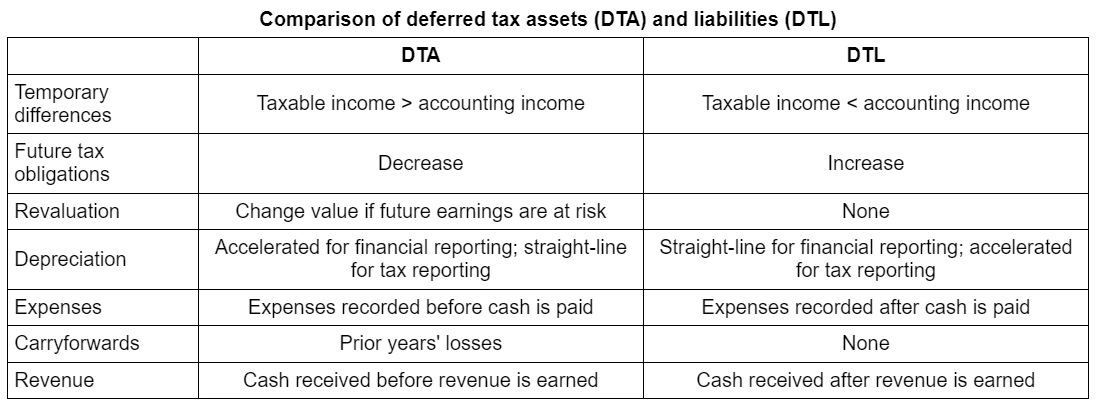

Deferred tax assets (DTA) arise when taxable profit is greater than accounting profit and taxes payable are greater than tax expense.

Deferred tax liabilities (DTL) arise when taxable profit is less than accounting profits and taxes payable are less than tax expense.

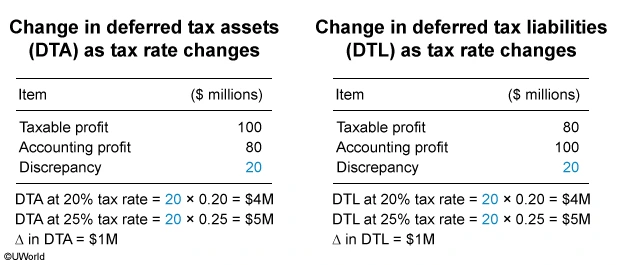

As illustrated above, at any given tax rate, deferred tax items can be calculated as the absolute difference between taxable profit and accounting profit, multiplied by the tax rate. Therefore, the sizes of DTA and DTL are directly related to the tax rate. As the tax rate increases, the value of deferred tax items also increase (Choices B and C).

Things to remember:

Deferred tax items can be calculated by multiplying the absolute difference between taxable profit and accounting profit by the applicable tax rate. Therefore, the sizes of deferred tax assets and deferred tax liabilities are directly related to the tax rate. As the tax rate increases, the value of deferred tax items also increases.

{kind=link}