Passage

Compass Engineering's board of directors is deciding between cash dividends or a share repurchase program as a method to begin returning cash to shareholders. Liam Fischer, a member of the board, states that both cash dividends and share repurchases have certain advantages that should be considered:

Advantage 1: Share repurchases tend to be more flexible. Although dividends can be raised, lowered, or suspended, they appear to create an expectation among investors that the distribution will continue in the future. Share repurchases do not seem to create the same expectation.

Advantage 2: If the tax rates for capital gains and dividends are the same, and the information coefficient is the same, then shareholders' wealth will be greater with cash dividends since all shareholders receive cash.

Alicia Wu, the chairman of the board, indicates that Compass should review the long-term trends in the country (the United Kingdom) before deciding.

After deliberation, the board favors a share repurchase program. Jessica King, another member of the board, is concerned about the effect of share repurchases on Compass' EPS. She collects the following data for 20X2:

| Exhibit 1 Compass' Financial and Market Information for Proposed Share Repurchases | |

|---|---|

| Net income (Millions) | £650 |

| Cash on hand (Millions) | £500 |

| Shares outstanding (Millions) | 100 |

| Current share price | £115 |

| Expected purchase price | £125 |

| Pretax cost of debt | 6% |

| Tax rate | 20% |

In addition, King wonders what effect share repurchases have on companies' book values. She gathers data from three of Compass' peers who have made a share repurchase:

| Exhibit 2 Financial Information on Compass' Peers | ||||

|---|---|---|---|---|

| Peer 1 | Peer 2 | Peer 3 | ||

| Net income | 150 | 300 | 350 | |

| Book value of equity | 3,000 | 5,000 | 6,500 | |

| Shares outstanding | 500 | 600 | 650 | |

| Value of shares repurchased | 90 | 80 | 310 | |

| Number of shares repurchased | 15 | 10 | 30 | |

| After-tax cost of debt | 5.5% | 6.0% | 5.0% | |

The board members then discuss the best approach for Compass to repurchase shares. King has identified two possible scenarios, both using the same amount to repurchase shares:

Scenario 1: Purchase shares using all cash on hand.

Scenario 2: Purchase shares with funds from an issuance of debt.

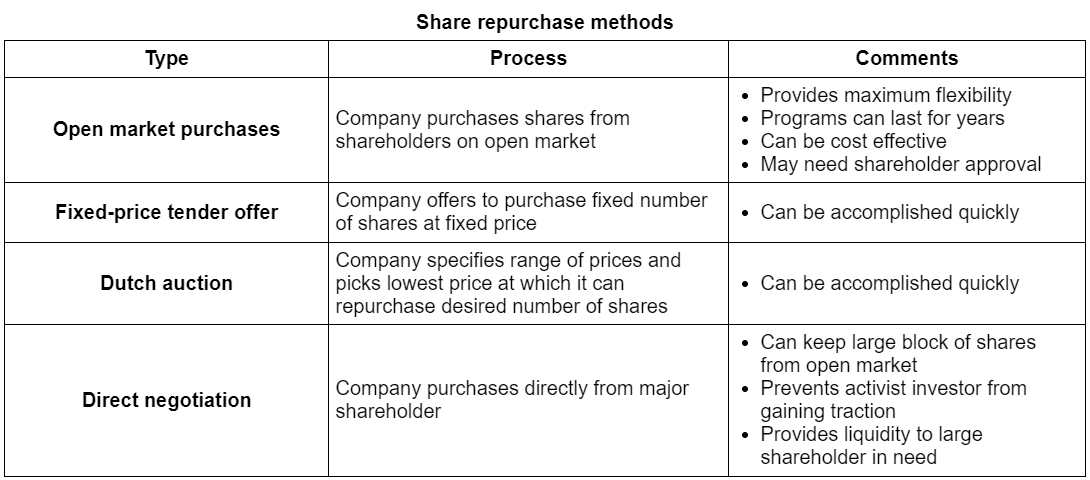

Wu states that her preference is to choose a method by which the company can control the process and execute it quickly. She also prefers a process that would allow Compass to discover the minimum price at which it can repurchase the desired number of shares.

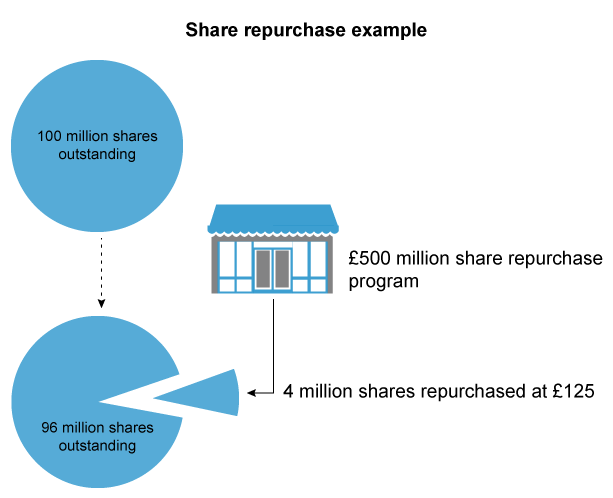

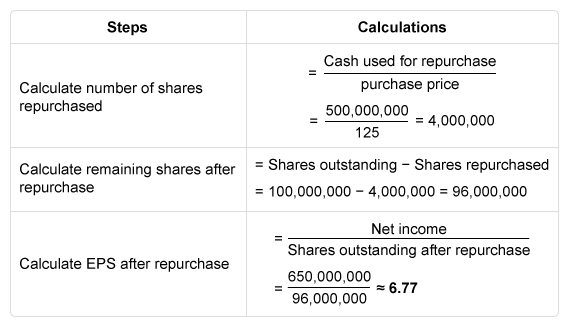

Based on Scenario 1 and Exhibit 1, a share repurchase would cause Compass' 20X2 EPS to be closest to:

Share repurchases are a popular alternative to cash dividends for returning cash to shareholders. Repurchases allow companies to purchase shares currently being held by shareholders using one of several methods. Once repurchased, the shares are either held for reissue (ie, treasury shares) or retired (ie, canceled shares).

The repurchase leaves fewer shares for investors to hold (ie, shares outstanding), which often results in a change to a company's per-share financial ratios (eg, EPS). Like dividends, share repurchases are made using corporate cash, whether the cash is on hand or obtained through the issuance of new debt.

- When cash on hand is used, EPS always increases.

- When new debt is issued, the change in EPS depends on the company's after-tax cost of debt and its earnings yield.

In this question, Compass' EPS following the share repurchase would be £6.77, calculated below.

(Choice A) £6.72 results from incorrectly applying the company's tax rate to the cash used to repurchase shares, arriving at cash of £400 million [£500 million × (1 − 0.2)].

(Choice C) £6.80 incorrectly uses the company's share price instead of the purchase price to calculate the number of shares repurchased. Companies do not always repurchase shares at the market price.

Things to remember:

Share repurchases are a popular alternative to cash dividends. They often result in a change to a company's per-share financial ratios. When cash on hand is used for a repurchase, EPS will always increase. When new debt is issued instead, the change in EPS depends on a company's after-tax cost of debt and its earnings yield.

{kind=link}