Portfolio Management: What to Expect in the CFA Level 1 Exam

The Portfolio Management (PM) topic holds a relatively lower weight on the Level 1 CFA exam, along with Derivatives and Alternative Investments. It’s crucial for you to recognize that PM is not any less significant than heavily weighted subjects such as Financial Statement Analysis (FSA). Instead, PM is a more intricate subject that builds upon fundamental concepts introduced earlier in the CFA Program.

As you progress through the CFA Program, the importance of PM grows, becoming over half of the Level 3 exam. Therefore, you should regard the lower-weighted content on Level 1 as a primer for this essential CFA exam topic. Establishing a strong foundation in PM is pivotal for achieving success and obtaining a CFA charter.

Exam Weighting

The topic weighs 8-12% of the L1 total exam content, so approximately 15-21 of the 180 questions focus on this topic.

| No. of Learning Modules | No. of Formulas |

|---|---|

| 6 | ca. 50 |

Syllabus, Readings, and Changes

The 2025 PM syllabus spans 6 learning modules and contains 40 learning outcome statements (LOS), with its main focus on portfolio planning and management.

Overview

Diversification of investments within a portfolio enables risk reduction while maintaining reward potential. An essential initial step in the portfolio management process involves creating a tailored Investment Policy Statement (IPS) that aligns with the client’s specific requirements. This process is followed by asset allocation, security analysis, portfolio construction, ongoing monitoring, rebalancing, performance evaluation, and reporting.

The reading introduces portfolio management and the asset management industry. You will become familiar with the portfolio management process and the financial needs of various investors. The material also covers mutual funds and other pooled investment instruments.

Portfolio Risk and Return: Part I

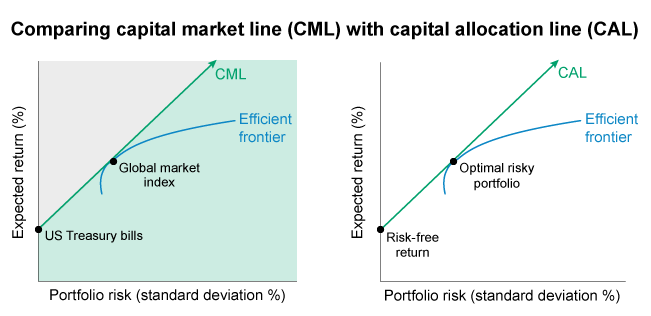

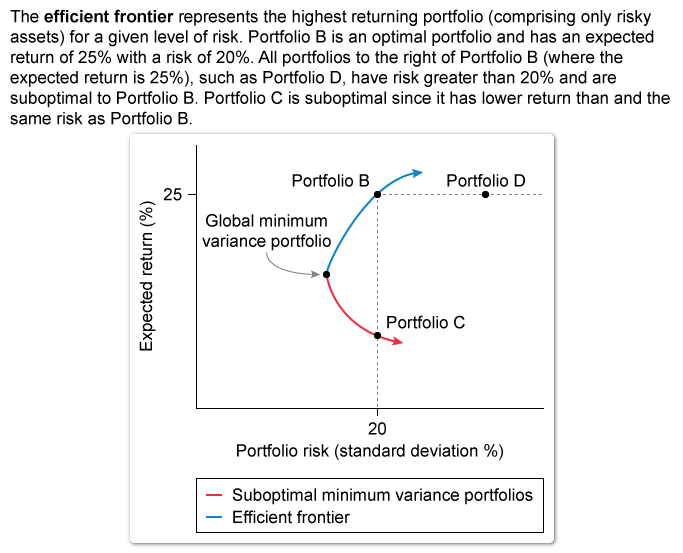

The most critical factors in portfolio development are the risk and return of individual assets, and the most efficient portfolios optimize that trade-off for the investor.

The reading examines the characteristics of assets as they relate to risks and returns. You will study risk aversion, the computation of portfolio risk, and the theory behind the choices of optimal risky portfolios.

Portfolio Risk and Return: Part II

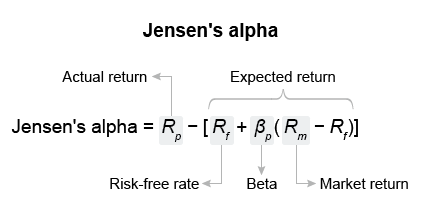

The reading dives deeper into the nuances of portfolio risk and return by examining the computation of risk, systematic and unsystematic risk, the capital asset pricing model (CAPM), and the role of correlation in diversifying risk. You will study various risk-related models and how risk influences portfolio valuation.

Basics of Portfolio Planning and Construction

A common theme reiterated throughout the CFA Level 1 PM topic is understanding a client’s situation and goals. While financial professionals categorize investors into broad groups, variations remain within these groups.

The reading examines the portfolio construction process with particular attention to client-centered planning. You will learn more about the investment policy statement and the portfolio construction process.

Behavioral Biases of Individuals

Human irrationality befuddles even the most realistic models. People often rely on their biases when making judgments and decisions. Behavioral finance challenges the assumptions of traditional economic and financial theories by accounting for this irrationality.

The reading examines the possible consequences of cognitive errors and emotional biases and how to mitigate their negative effects. You will also study how the aggregate expression of individual biases manifests as market anomalies.

Introduction to Risk Management

Investment decisions are always made within an environment of uncertainty. Risk management is a skill that allows investors to navigate this environment. To do this, investment advisers and managers must be able to identify appropriate risk measures and keep risks aligned with investment goals.

The reading offers a broad enterprise and portfolio risk management process overview. You will learn about risk governance, tolerance, and measuring and managing risk.

Portfolio Management: Overview

This topic centers on comprehending the portfolio investment approach and detailing the steps involved in portfolio management. It also examines diverse investor profiles, emphasizing their unique traits and requirements. The discourse extends to clarifying defined contribution and defined benefit pension plans, delving into facets of the asset management sector. Additionally, it encompasses an overview of mutual funds, accompanied by a comparative analysis of other pooled investment options.

Sample Questions and Answers

These sample questions are typical of the probing multiple-choice questions on the L1 exam. During the exam, you have about 90 seconds to read and answer each question, carefully designed to test knowledge from the CFA curriculum. UWorld’s question bank is built to expose you to exam-like questions and illustrate and explain the concepts tested thoroughly.

Portfolio Management: What to Expect in the CFA Level 2 Exam

The Level 2 Portfolio Management syllabus discusses the creation, trading, costs, and risks of exchange-traded funds (ETFs) and how to use them strategically. You explore the connections between financial markets and the real economy and are introduced to the Fundamental Law of Active Management. The material wraps up with case studies of portfolio management, which demonstrate how securities trading relates to the investment process.

Exam Weighting

The CFA PM topic weighs 10-15% of the total exam content, so approximately 8-12 of the 88 CFA Level 2 exam questions or 2-3 of the 22-item sets focus on this topic.

| No. of Learning Modules | No. of Formulas |

|---|---|

| 6 | ca. 70 |

Syllabus, Readings, and Changes

The CFA Level 2 Portfolio Management (PM) syllabus encompasses 6 learning modules and 52 learning outcome statements. The Level 2 exam focuses on Exchange Trades, Market Risks, Investments, and Portfolio Management. Notably, for the 2025 exam, specific LOS from 2023 have either been consolidated into other readings or omitted.

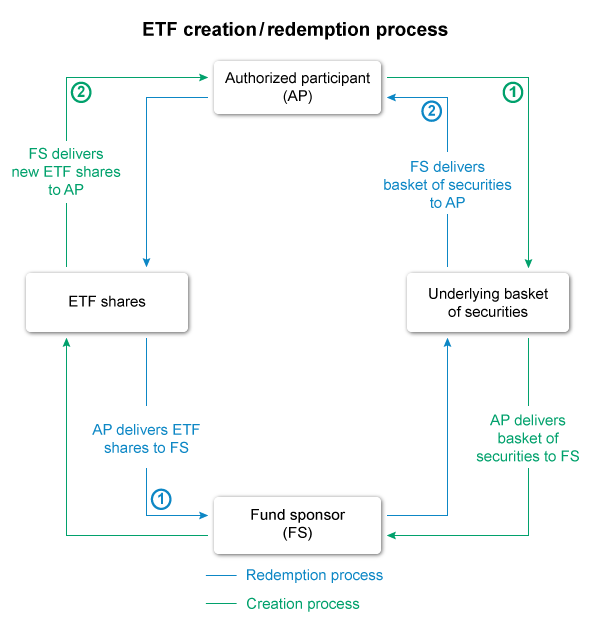

Exchange-traded Funds: Mechanics and Applications

Exchange-traded funds (ETFs) were developed as an alternative to mutual funds based on the Modern Portfolio Theory discussed in the CFA curriculum. They have grown in popularity due to access, relatively low cost, transparency, and the diversity of available assets. ETFs are also typically more tax-efficient than mutual funds, making them more helpful in diversifying positions and portfolios.

The reading introduces the primary and secondary markets for ETFs and how ETFs are used effectively for portfolio development. You will also examine the risks and costs of ETFs and other important considerations for investors.

Using Multifactor Models

Multifactor models allow financial analysts to construct a more precise and nuanced view of risk than possible with a single-factor approach. This has made multifactor models a dominant investment practice for measuring and navigating risk.

The reading provides a background on the modern portfolio theory of multifactor models.You will be introduced to arbitrage pricing theory, various multifactor models, and their applications.

Measuring and Managing Market Risk

Market risk may mean fluctuations in stock prices, interest rates, exchange rates, or commodity prices. Risk management allows financial analysts to align risks with investment goals by classifying and measuring such risks. This is done through financial models, experience, and good judgment.

The reading provides a foundation for understanding and assessing Value at Risk (VaR). You will learn about the constraints in risk management and sensitivity measures used for equities, fixed-income securities, and options.

Backtesting and Simulation

Backtesting is the practice of simulating the performance of an investment strategy without risking capital. This allows financial analysts to test hypotheses using historical data to simulate results they can analyze for return. Backtesting and simulation have become increasingly popular in quantitative investing due to the rise in big data and other associated technological developments.

The reading introduces backtesting techniques. You will learn how these tools increase the usefulness of otherwise “random” data.

Economics and Investment Markets

Financial market activity is intimately interwoven with the overall state of the economy. Through financial markets, savers can defer consumption, providing governments and corporations greater access to capital.

The reading explores the connection between the real economy and financial markets and demonstrates the usefulness of economic analysis in the valuation of securities and their aggregates. You will review how the economy influences the prices of various forms of debt, equity, and credit.

Analysis of Active Portfolio Management

Modern portfolio theory (MPT) has its roots in the 1952 Markowitz framework. It has since evolved into the dominant framework for discussing and applying the principles of risk and return in portfolio management. Since 1952, various models, concepts, terminology, and mathematics have been combined with the Markowitz framework to create the MPT.

You are expected to have an understanding of basic portfolio theory (from Level 1) before reading in this section. The reading introduces the mathematics of “value-added” through active portfolio management, compares various risk measurements, and provides examples of active portfolio management strategies in equity and fixed-income markets.

Sample Questions and Answers

These sample questions are typical of the L2 exam’s complexity and depth – formatted as item sets, with a vignette to deliver a scenario that tests the CFA L2 exam curriculum. On the actual exam, each vignette applies to 4 questions. We’ve added a few additional ones for you to practice with. Be sure to review the illustrated explanations we’ve provided for each question. UWorld’s question bank is designed to expose you to exam-like questions and explain the concepts tested thoroughly.

{kind=link}

{kind=link}

Latest Changes in the Level 3 Curriculum

For the 2025 CFA Program Level 3, CFA Institute (CFAI) has introduced substantial enhancements and expansions, marking 1 of the most significant developments since the program’s inception. This year features the debut of specialized pathways in Private Wealth, Private Markets, and Portfolio Management, allowing you to tailor your learning to align closely with your career aspirations. Each pathway builds on a robust common core, enriched with specialized content designed to deepen expertise in your chosen area. As you delve into these new pathways, detailed descriptions of each can be found seamlessly integrated within our Level 3 curriculum topic outline guide.