What to Expect in CFA Level 1 Alternative Investments?

This topic explores Alternative Investments, including hedge funds, private equity, real estate, commodities, and infrastructure. In this curriculum, CFAI defines Alternative Investments, the characteristics they have in common, and their usefulness in creating diversification and higher returns.

Exam Weighting

The CFA Level I Alternative Investment weighs 7-10% of the total exam content, so approximately 13-18 CFA Level I exam questions focus on this topic.

| Topic Weight | No. of Learning Modules | No. of Formulas | No. of Questions |

|---|---|---|---|

| 7-10% | 7 | Nearly 15 | 13-18 |

Level 1 Alternative Investments 2024 Syllabus, Readings, and Changes

The CFA Level 1 exam includes 7 total learning modules for 2024. Numerous new texts have been added to the curriculum at all three levels, substantially expanding the focus on the topic area of Alternative Investments. One other change for 2024 is the Introduction to Digital Assets.

| No. of Learning Modules – 7 | No. of LOS – 22 | |

|---|---|---|

|

Summary

This reading provides a comprehensive introduction to Alternative Investments. Alternative investments are asset classes or investment vehicles that supplement traditional long-only positions in stocks, bonds, and cash. Alternative investments include five main categories: hedge funds, private capital, natural resources, real estate, and infrastructure.

|

||

This significant change expands the discussion of alternatives and gives more information on how to use them in an investment strategy. In-depth exploration of alternative asset classes, risk management, and alternative investment structures are combined with fundamental knowledge to produce a simplified learning experience.

Alternative Investment Features, Methods, Structures, Performance, and Returns

This topic focuses on understanding the features and categories of alternative investments. It delves into the distinctions between direct investment, co-investment, and fund investment methods within alternative investments.

Additionally, the discussion explores prevalent investment ownership and compensation structures commonly employed in alternative investments.

Investments in Private Capital: Equity and Debt

Since they may be infrequently and/or privately traded, pricing, valuation, and performance can be much more difficult to assess for alternative investments. This learning module explores the factors, models, and circumstances that impact performance evaluation.

Private Capital, Real Estate, Infrastructure, Natural Resources, and Hedge Funds

This learning module looks at the various categories of alternative investments and their specific characteristics, risks, and returns.

Introduction to Digital Assets

This topic explores the financial applications of distributed ledger technology. It encompasses an explanation of the investment features of digital assets and provides a comparative analysis with other asset classes. Furthermore, the discussion covers various investment forms and vehicles utilized in digital asset investments. Additionally, it involves the analysis of sources of risk, return, and diversification within the landscape of digital asset investments.

CFA Alternative Investments Level 1 Sample Questions and Answers

The sample questions are typical of the probing multiple-choice questions on the L1 exam. During the exam, you have about 90 seconds to read and answer each question, carefully designed to test knowledge from the CFA Curriculum. UWorld’s question bank is built to expose you to exam-like questions and illustrate and explain the concepts tested thoroughly.

What to Expect in CFA Level 2 Alternative Investments?

These readings focus on real estate, private equity, and commodities. The readings describe real estate investments, both private and public, and methods for analysis and evaluation. Private equity, including venture capital and leveraged buyouts, is examined from the perspectives of both a private equity firm evaluating equity portfolio investments and an investor considering participation in a private equity fund. Strategies involving commodity hedging are also discussed.

The CFA Level 2 Alternative Investment (AI) is not only fundamental to passing CFA Level 2 but to succeeding in the CFA overall.

Exam Weighting

CFA Alternative Investment has a weighting of 5-10% of the total exam content, such that approximately 4-8 questions or 1-2 item sets focus on this topic.

| Topic Weight | No. of Learning Modules | No. of Formulas | No. of Questions |

|---|---|---|---|

| 5-10% | 4 | Around 20 | 4-8 |

Level 2 Alternative Investments 2024 Syllabus, Readings, and Changes

The 2024 CFA Level 2 exam comprises four learning modules. Notably, Private Equity Investments has been removed from the readings, and Hedge Fund Strategies has been introduced into the curriculum.

| No. of Learning Modules – 4 | No. of LOS – 29 | |

|---|---|---|

|

Summary

These learning modules focus on the following categories of Alternative Investments: real estate, private equity, and commodities. Real estate investments, both private and public, are described, and methods for analysis and evaluation are presented. Private equity, including venture capital and leveraged buyouts, is examined from both the perspectives of a private equity firm evaluating equity portfolio investments and of an investor considering participation in a private equity fund. |

||

Although it is commonly known that real estate contributes significantly to a balanced portfolio’s diversification, applicants should be aware of how significantly the risk profile of real estate investments varies depending on the type of asset. The “Real Estate Investments” material describes the risk profile of real estate debt vs equity (as a lender or owner of mortgage-backed securities), primarily focusing on commercial real estate.

Overview of Types of Real Estate Investments

Real estate property holds substantial importance within investment portfolios, offering an appealing source of current income.

This learning module provides a comprehensive comparison of the features, classifications, primary risks, and fundamental structures of both public and private real estate investments. It also delves into the roles real estate plays in portfolios and the factors determining its economic value.

Furthermore, the module explores various commercial property types, shedding light on their unique investment traits. It covers the due diligence procedures applicable to both private and public equity real estate investments. Additionally, it addresses real estate investment indexes, including their construction methods and potential biases

Investments in Real Estate through Publicly Traded Securities

These learning modules compare various characteristics, classifications, and risks for public and private real estate investments. They also describe the valuation principles and approaches for pricing alternative assets along with discussion on the advantages and disadvantages of investing in real estate through publicly traded securities compared to private vehicles.

Introduction to Commodities and Commodity Derivatives

This reading provides a discussion of commodities and commodity futures, including scenarios of contango and backwardation for futures prices.

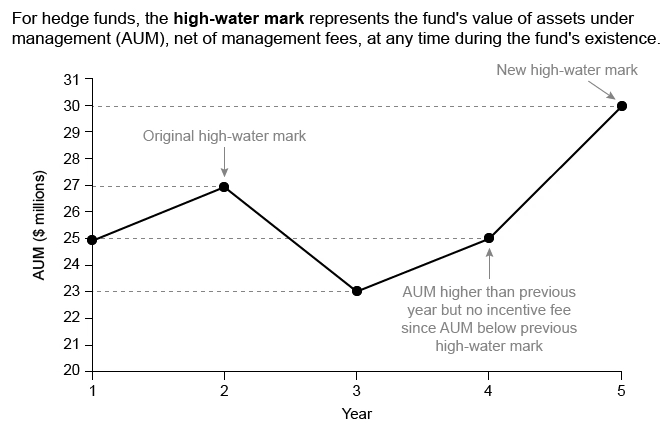

Hedge Fund Strategies

This topic focuses on classifying hedge fund strategies, including equity-related, event-driven, relative value, opportunistic, specialist, and multi-manager strategies. It delves into the investment characteristics, strategy implementation, and the role each plays in a portfolio.Additionally, the discussion encompasses how factor models can be utilized to comprehend hedge fund risk exposures and evaluates the impact of allocating to a hedge fund strategy within a traditional investment portfolio.

CFA Alternative Investments Level 2 Sample Questions and Answers

The provided sample questions exemplify the level of complexity and depth encountered in the Level 2 exam. They are presented as item sets, each accompanied by a vignette that creates a scenario designed to assess your understanding of the CFA Level 2 Curriculum. It’s worth noting that on the actual exam, each vignette applies to four questions, but we’ve included a few extra questions to enhance your learning experience. We strongly recommend reviewing the detailed explanations provided for each question. UWorld’s question bank is specifically designed to familiarize you with exam-style questions and provide comprehensive explanations to help you grasp the tested concepts thoroughly.

Passage

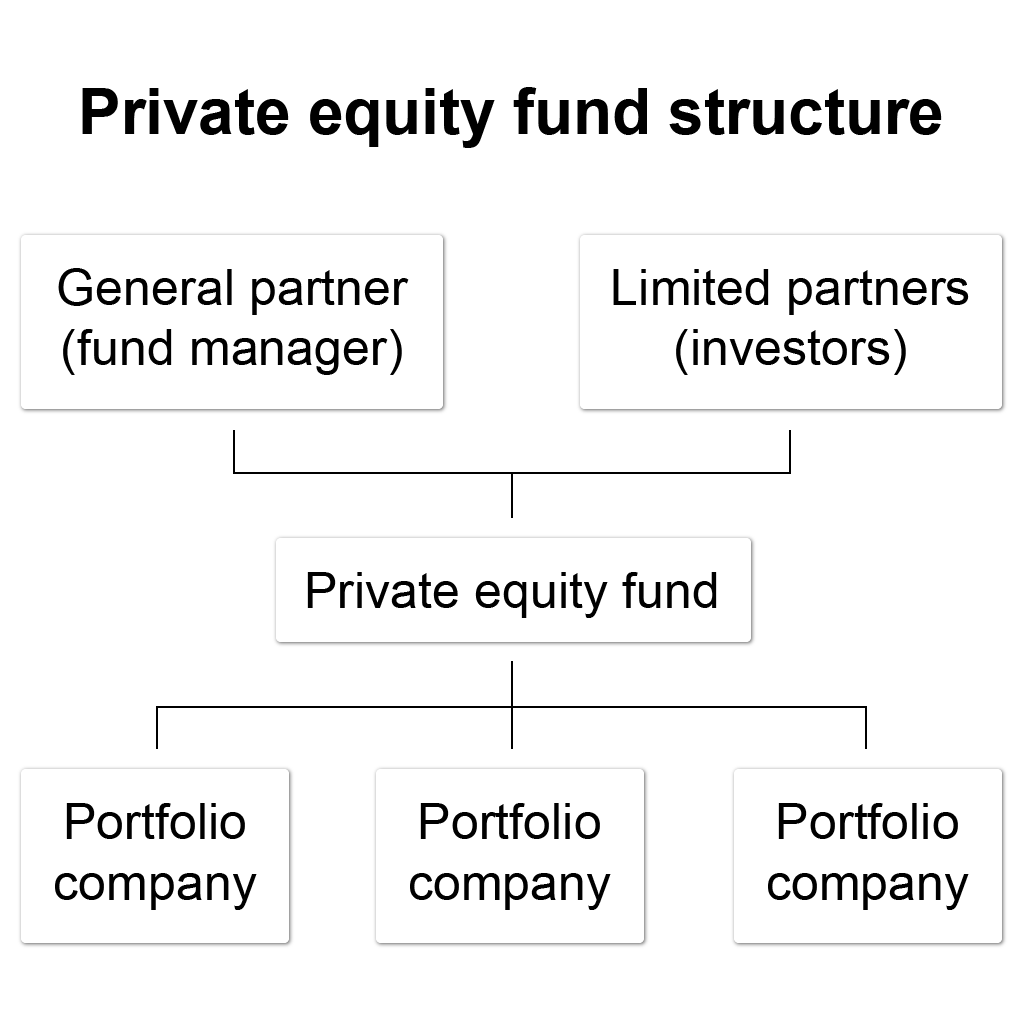

Chao Li is a vice president at Tailwind Capital, a private equity (PE) firm. He is currently raising £100 million for Tailwind Fund A. Li meets with An Heng, an associate at Insular Insurance Co., a potential institutional investor. In their meeting, Li explains the general structure of PE funds to Heng:

- Statement 1: The limited partners (LPs) and the general partner (GP) in a private equity fund participate in managing the fund.

- Statement 2: The GP is entitled to carried interest, which is typically a percentage of the fund’s profits after management fees.

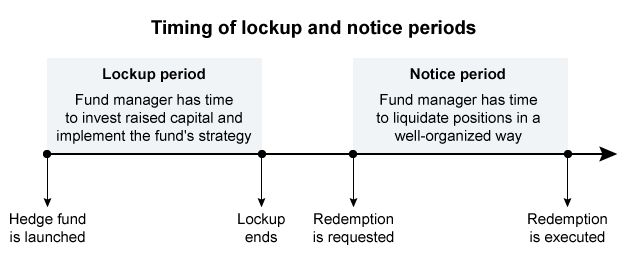

- Statement 3: PE funds are closed-end funds, so LPs can redeem their investments only at specified times.

Heng says, “I understand there are costs associated with investing in PE, such as significant performance fees, dilution costs whenever the PE firm starts new funds, and annual audit costs. And I know that there are some agency risks involved with investing in a PE fund. Is there a governance provision that would address GP gross negligence?”

Subsequently, Li raises the full £100 million for Fund A. One of the fund’s investments is ModernWare, an online services company. The initial investment is £20 million: £13 million in debt, £2 million in preferred equity, and £5 million in the PE fund’s equity. Tailwind plans to sell ModernWare 5 years from now and plans to reduce the debt balance by £10 million by the time of exit. The promised return for the preferred equity holders is 15%.

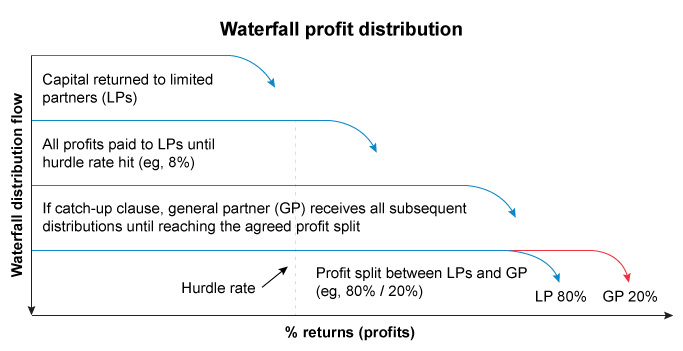

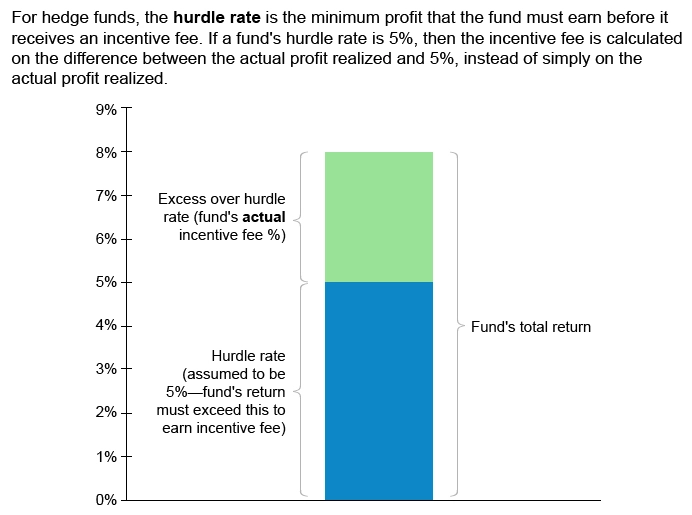

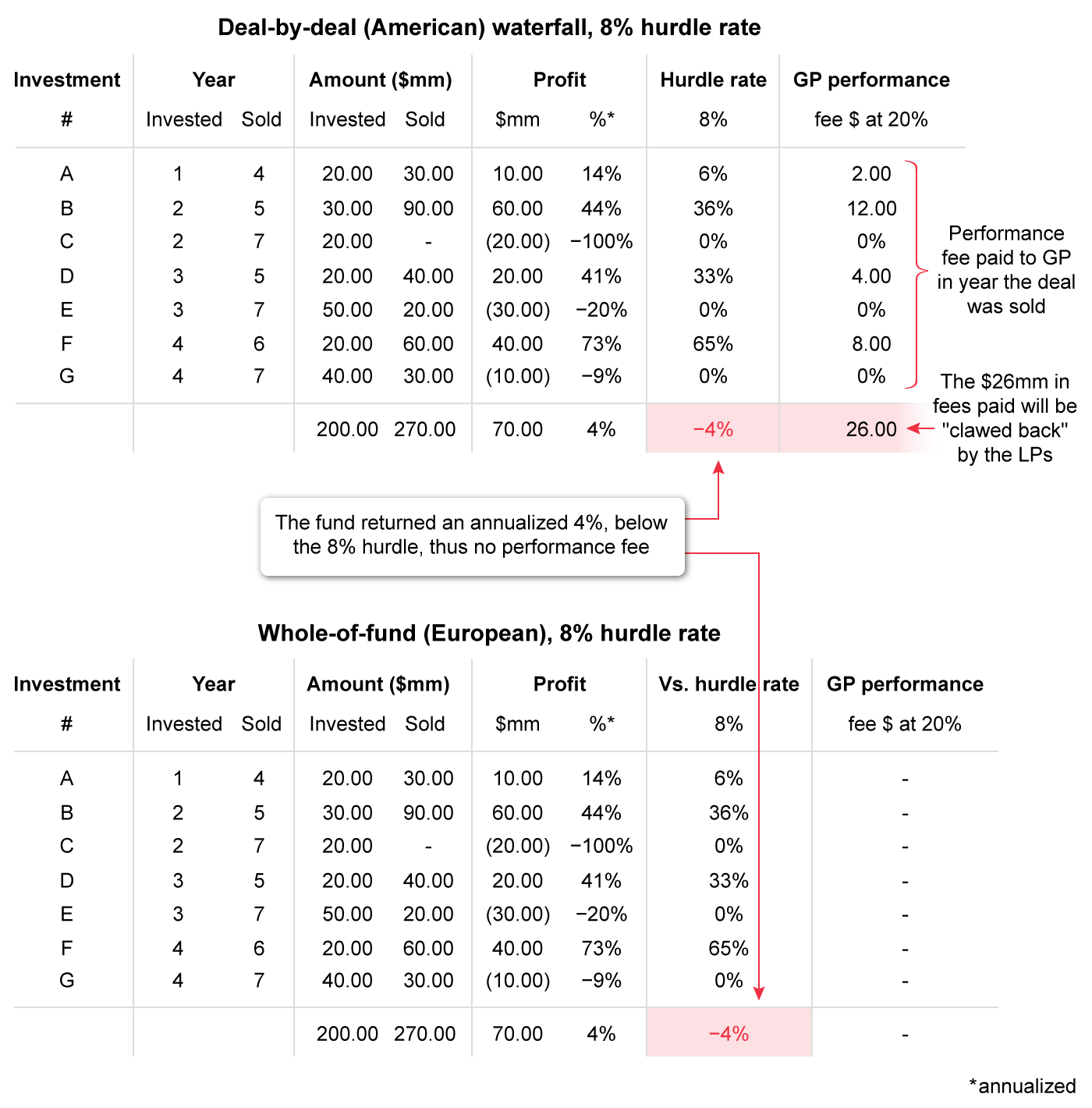

Several years after the fund’s inception, Tailwind exits two investments: StoneWare and BronzeWare (Exhibit 1). Carried interest to the GP is accrued on a deal-by-deal basis and equals 20% of the profits from each exit. The hurdle rate is 10%. When a deal’s IRR is above the hurdle rate, carried interest is accrued; when a deal’s IRR is below the hurdle rate, a clawback penalty amount is accrued if there is a loss.

| Exhibit 1 Investment Exits | |||

|---|---|---|---|

| Company | Initialinvestment (at T = 0) | Profit from exit (£ millions) | Exit year |

| StoneWare | 8 | 3 | T = 3 |

| BronzeWare | 5 | -1 | T = 4 |

Twelve years after the fund’s inception, Li meets with Heng again to review Fund A’s performance, shown in Exhibit 2.

| Exhibit 2 Tailwind Fund A Performance | ||||||

|---|---|---|---|---|---|---|

| Committed capital (£ millions) | Paid-in capital | Net IRR(%) | Distributions to paid-in capital | Residual value to paid-in capital | Total value to paid-in capital | Maturity |

| 200 | 190 | 25.0% | 1.40 | 1.45 | 2.85 | 12 years |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

What to Expect in CFA Level 3 Alternative Investments?

CFA Level 3 Alternative Investments delves into the unique regulatory and investment characteristics of major hedge fund strategy categories. It also delves into the role of alternative assets within a multi-asset portfolio and how they can help mitigate the risk associated with long-only equity investments. The curriculum explores various approaches to asset allocation when incorporating alternatives, whether through traditional methods or using risk- or factor-based approaches. Notably, there are two out of the 35 (5.7%) Level 3 readings dedicated to Alternative Investments.

Candidates will explore these concepts and principles in greater depth compared to the broader coverage in the CFA Institute Level 2 Alternative Investments curriculum.

Exam weighting

The CFA Alternative Investment curriculum has a weighting of 5-10% of the total exam content so approximately 1-2 item sets and 4-8 essay questions will focus on this topic.

| Topic Weight | No. of Readings | No. of Formulas | No. of Questions |

|---|---|---|---|

| 5-10% | 2 | Around 5 | 8-13 |

Level 3 Alternative Investments 2024 Syllabus, Readings, & Changes

The CFA Level 3 exam allocates approximately 5.7% of its content to Alternative Investments, featuring two readings. While there were 17 Learning Outcome Statements (LOS) in 2023, the 2024 curriculum streamlines this to 16 LOS in the Alternative Investments section.

| No. of Readings – 2 | No. of LOS – 16 |

|---|---|

|

Summary

Presents distinctive regulatory and investment characteristics of the major categories of hedge fund strategies. Discuss the role alternative assets play in a multi-asset portfolio and explore how alternatives may mitigate long-only equity risk. Discusses approaches to asset allocation when incorporating Alternatives in the opportunity set whether using the traditional asset class approach or risk or factor-based investing. |

|

Hedge Fund Strategies

This reading discusses important hedge fund categories as well as the investment characteristics of six main hedge fund strategies: equity-related, event-driven, relative value, opportunistic, specialist, and multi-manager strategies.

Asset Allocation to Alternative Investments

This study discusses the potential benefits of adding Alternative Investments to a portfolio of traditional investments that typically include debt and equity. Characteristics of Alternative Investments that impact asset allocation decisions are discussed. Factor-based optimization versus mean-variance optimization is compared along with a discussion of liquidity concerns and time horizon regarding Alternative Investments’ suitability.