What to Expect in CFA Level 1 Equity Investments

This section delves into the critical insights and methodologies employed in formulating investment recommendations and decisions. It centers on the principles of fundamental analysis, a cornerstone in determining investment choices. The course provides an in-depth exploration of techniques used to estimate a company’s intrinsic value. Additionally, it offers insights into the workings of an effective financial system, addressing topics like market efficiency and diverse strategies for appraising both public and private equity.

The Equity Investments (EI) module represents a significant Level 1 CFA examination component. Mastery of this topic is pivotal for excelling in the initial stage and crucial for overall success in the CFA Program.

Exam Weighting

CFA Institute’s Level I Equity Investments topic has an exam weight of 11-14% of the total exam content, so approximately 20-25 of the 180 CFA Level 1 exam questions focus on this topic.

| No. of Learning Modules | No. of Formulas |

|---|---|

| 6 | Nearly 15 |

Level 1 Equity Investments Syllabus, Readings and Changes

The CFA Level 1 Equity syllabus encompasses 8 learning modules with a total of 66 learning outcome statements (LOS). Noteworthy changes include the expansion of Company Analysis into 2 distinct modules and the enhancement of Industry Analysis to incorporate Competitive Analysis.

| No. of Learning Modules – 8 | No. of LOS – 66 | |

|---|---|---|

|

Summary

A structural overview of financial markets and their operating characteristics is provided. Overview includes markets for equities, fixed income, derivatives, and alternative investments. Various asset types, market participants, and types of trades within these markets and ecosystems are described. The calculation, construction, and use of security market indexes are discussed together with market efficiency: how well market prices reflect available information.

|

||

Market Organization and Structure

This reading provides an overview of various types of markets and the actors who participate in them. The overview includes markets for equities, fixed income, derivatives, and alternative investments.

Security Market Indexes

This reading focuses on different types of indexes, how they are constructed, and what they are used for.

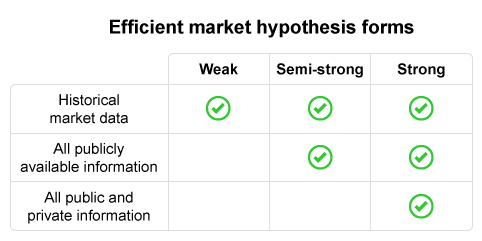

Market Efficiency

This reading presents a detailed discussion on whether and/or how effectively market prices reflect the intrinsic value of securities.

Overview of Equity Securities

This reading provides a qualitative analysis of the features that distinguish equity securities from other asset classes and their roles in the capital markets.

Company Analysis: Past and Present

This course prioritizes Company Analysis: Past and Present, equipping you to articulate elements in a research report, determine a company’s business model, and evaluate revenue factors such as pricing power. It also guides the assessment of operating profitability, working capital efficiency, and insights into financial decision-making regarding capital investments and structure.

Industry and Competitive Analysis

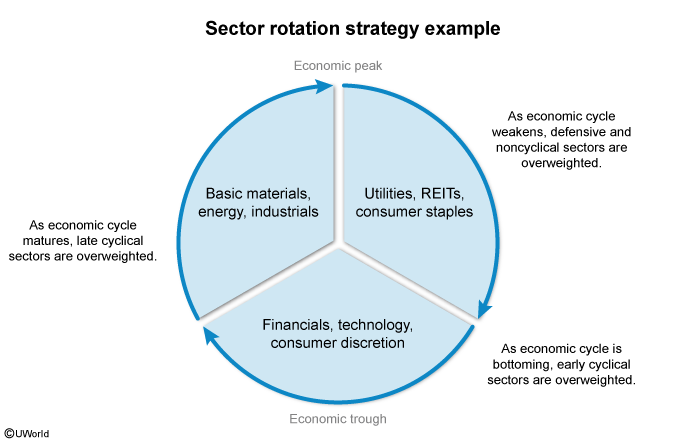

Focused on Industry and Competitive Analysis, this course equips you to articulate analysis purposes and steps. It covers industry classification methods, sizing, growth, profitability trends, and market share. Analyzing industry structure and external factors is emphasized, employing Porter’s Five Forces and Political, Economic, Sociological, Technological, Legal, and Environmental (PESTLE). You will also evaluate competitive strategy and company positioning.

Company Analysis: Forecasting

You will learn principles and approaches for forecasting a company’s financials, including revenue, operating expenses, and capital structure. The course also explores the strategic use of scenario analysis in forecasting.

Equity Valuation: Concepts and Basic Tools

You will learn to evaluate securities, categorize equity valuation models, and calculate intrinsic values using discount models and price multiples. Additionally, the course covers understanding dividend structures, including regular and extra dividends, stock dividends, stock splits, reverse stock splits, and share repurchases. The use of enterprise value multiples and asset-based valuation models for estimating equity value is also explored.

For a more comprehensive discussion visit the CFA Level 1 syllabus page.

CFA Equity Investments Level 1 Sample Questions and Answers

These sample questions are typical of the probing multiple-choice questions on the CFA L1 exam. During the exam, you have about 90 seconds to read and answer each question, carefully designed to test knowledge from the CFA curriculum. UWorld’s question bank is built to expose you to exam-like questions and illustrate and explain the concepts tested thoroughly.

What to Expect in CFA Level 2 Equity Valuation

The CFA Level 2 Equity Valuation (EV) curriculum, formerly known as CFA Equity Investments (EI), is one of the more heavily weighted topics, with 6 learning modules dedicated to EV. This topic is not only fundamental to passing Level 2 but succeeding on the CFA Exam overall. You will dive deeper into the concepts and principles presented in the Level 1 curriculum.

Exam Weighting

The CFA Equity Valuation weighs 10-15% of the total exam content so that approximately 8-12 questions or 2-3 item sets of the CFA Level 2 exam focus on this topic.

| No. of Learning Modules | No. of Formulas |

|---|---|

| 6 | Around 100 |

Level 2 Equity Valuation Syllabus, Readings, and Changes

The data, examples, and references in all six learning modules in the Equity Valuation topic area have been refreshed, but the readings’ content remains unchanged. For a more comprehensive discussion of LOS visit the official CFAI Level 2 Curriculum Changes page.

| No. of Learning Modules – 6 | No. of LOS – 76 | |

|---|---|---|

|

Summary

The course begins with fundamental equity valuation concepts, exploring value definitions and application of models. Key return measures, including equity risk premium and derived required return, are discussed. Models like discounted cash flow (DCF) and the dividend discount model (DDM) are covered, with a focus on alternative methods like the free cash flow model. Relative valuation, using multiples, and residual income valuation are explored. The session concludes with approaches for valuing private company equity. |

||

Equity Valuation: Applications and Processes

This reading discusses the various definitions of value and the application of equity valuation techniques. A 5-step equity valuation process is described with the presented 3 main categories of equity valuation models (absolute, relative, and total entity).

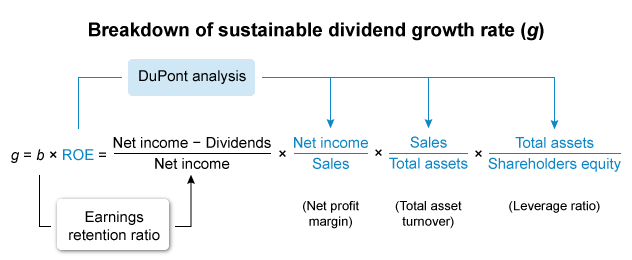

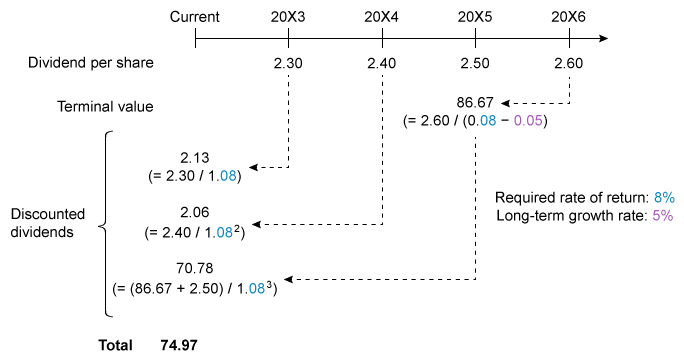

Discounted Dividend Valuation

This learning module explains the calculation and interpretation of the value of common stock using the dividend discount model (DDM) and the Gordon growth model for single and multiple holding periods. It explains the models’ underlying assumptions, interprets the implied growth rate of dividends, and compares intrinsic value and the market value based on the DDM.

Free Cash Flow Valuation

This learning module compares the free cash flow to the firm (FCFF) and free cash flow to equity (FCFE) approaches to valuation. It describes approaches for forecasting FCFF and FCFE and compares the FCFE model and dividend discount models. This reading also explains the single-stage (stable-growth), 2-stage, and 3-stage FCFF and FCFE models and justifies the selection of the appropriate model given a company’s characteristics. It then describes how to estimate a company’s value using the appropriate free cash flow model.

Market-Based Valuation: Price and Enterprise Value Multiples

This learning module provides contrast on the valuation methods based on comparables and on forecasted fundamentals as approaches to valuation and explains economic rationales for each approach. The discussion includes rationales for and possible drawbacks to using alternative price multiples and dividend yield in estimates of intrinsic value.

Residual Income Valuation

This learning module describes, calculates, and interprets residual income and its uses in estimating the common stock’s intrinsic value, especially compared to other approaches. It explains the fundamental determinants of residual income and discusses the strengths and weaknesses of residual income models, including accounting issues in residual income model applications.

Private Company Valuation

This learning module describes issues of private business valuation. It explains the cash flow estimation issues and adjustments required to estimate normalized earnings and calculate the value of a private company using different approaches. Also included are discussions of the effects of discounts and premiums based on control and marketability on private company valuations.

CFA Equity Valuation Level 2 Sample Questions and Answers

These sample questions here are typical of the L2 exam’s complexity and depth – formatted as item sets, with a vignette to deliver a scenario that tests the CFA L2 curriculum. On the actual exam, each vignette applies to 4 questions. We’ve provided a few additional questions to get you comfortable with what you might see on the exam. Be sure to review the illustrated answer explanations we’ve provided for each question. UWorld’s question bank is designed to expose you to exam-like questions and explain the concepts tested thoroughly.

{kind=link}

What to Expect in CFA Level 3 Equity Investments?

Equity Investments does not exist as a separate topic area in Level 3. Equity concepts appear within Portfolio Management when constructing equity portfolios, evaluating factor exposures, assessing risk premia, or building return expectations.