What to Expect in CFA Level 1 Ethics

CFA Level 1 Ethics is the most heavily weighted topic on the exam at 15-20%. The topic introduces CFAI’s 6 Codes of Ethics and 7 Standards of Professional Conduct (the Code and Standards). You must use these Codes and Standards as a framework for ethical decision-making throughout your financial career. While there are no formulae to memorize, Ethics is commonly regarded as one of the most challenging CFA Level 1 topics due to its breadth of material and relatively subjective nature. The topic material closes with a short introduction to Global Investment Standards (GIPS). Some of this material is optional.

Exam Weighting

The CFA Ethics topic has an exam weighting of 15-20%, meaning that approximately 27-36 of the 180 CFA Level 1 exam questions focus on this topic.

| No. of Learning Modules | No. of Formulas |

|---|---|

| 5 | 0 |

Level 1 Ethics 2026 Syllabus, Readings, and Changes

CFA Level 1 exam has not seen much fluctuation with the ethics portion since last year. The minimal changes include merging 2 or more readings (now called learning modules) leading to lesser learning outcome statements (LOS) this year.

| No. of Learning Modules – 5 | No. of LOS – 21 | |

|---|---|---|

Summary Introduces the CFAI® Code of Ethics and Standards of Professional Conduct and how to apply such standards to particular situations. Concludes with an overview of the Global Investment Performance Standards (GIPS). | ||

Ethics and Trust in the Investment Profession

Financial analysis is about more than formulae and forecasting. Financial markets and businesses could not function without trust in individuals and institutions. This reading introduces the concept of investing as a profession and the importance of ethical behavior in investing. You will learn to create trust through maintaining standards, abiding by codes, and applying an ethical framework to your daily professional decisions.

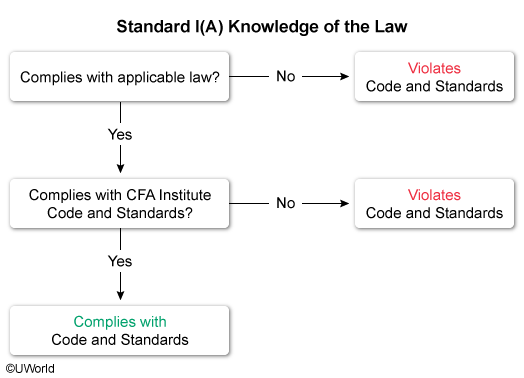

Code of Ethics and Standards of Professional Conduct

Students often struggle with Ethics because it relies more on subjectivity and intuition than formulae. However, the Standards of Practice Handbook makes the theoretical side of Ethics more concrete by providing guidance on common ethical dilemmas that investment professionals face on a daily basis.

This reading describes the importance of building a positive community of reputable investment professionals who strive to meet and surpass industry expectations. You will learn that Ethics is not just about an individual’s good choices but the aggregate of ethical decisions made by a community of members.

“Through members’ and candidates’ adherence to these principles as a whole, the integrity of and trust in the capital markets are improved.”

Guidance for Standards I-VII

You are expected to understand how to apply the Code of Ethics and Standards of Professional Conduct to real-world situations that they may face as professional financial analysts.

Guidance for Standards is broken down into 7 general sections, each with its own subcategories:

- Professionalism

- Integrity of Capital Markets

- Duties to Clients

- Duties to Employers

- Investment Analysis, Recommendations, and Actions

- Conflict of Interest

- Responsibilities as a CFA Institute Member or CFA Candidate

The readings will instruct you on procedures designed to prevent violations and conduct yourself appropriately in situations involving your professional integrity.

Introduction to the Global Investment Performance Standards (GIPS)

The Global Investment Performance Standards are voluntary ethical guidelines applied to investment performance reporting and designed by CFA Institute (CFAI) in partnership with GIPS Standards sponsors and industry experts. Investment firms and asset owners abide by GIPS as a commitment to transparency for investors.

This reading introduces GIPS standards and explains the reasoning behind their creation. You will become familiar with the benefits of industry-wide standards and their elevation of the community as a whole.

Ethics Application

This course prioritizes Company Analysis: Past and Present, equipping you to articulate elements in a research report, determine a company’s business model, and evaluate revenue factors such as pricing power. It also guides the assessment of operating profitability, working capital efficiency, and insights into financial decision-making regarding capital investments and structure.

Ethics Application

This reading allows you to exercise your newly acquired ethics thinking. You will apply your CFAI Code of Ethics and Standards of Professional Conduct knowledge to a series of real-world scenarios. After selecting an answer, the reading presents the correct response and the rationale behind it.

CFA Ethics Level 1 Sample Questions and Answers

These sample questions are typical of the probing multiple-choice questions on the L1 exam. During the exam, you have about 90 seconds to read and answer each question, carefully designed to test knowledge from the CFA curriculum. UWorld’s question bank is built to expose you to exam-like questions and illustrate and explain the concepts tested thoroughly.

What to Expect in CFA Level 2 Ethics

CFA Level 2 Ethics is one of the most heavily weighted topics on the exam at 10-15%. The topic material reiterates about 80% of the material found in the CFA Level 1 Ethics. Level 2 introduces the item set format for the entire exam, including Ethics. This form of testing ensures that you have a deeper understanding of the material.

Exam Weighting

The CFA Level 2 Ethics topic has an exam weighting of 10-15%, such that approximately 8-12 of the 88 CFA Level 2 exam questions or 2-3 item sets focus on this topic.

| No. of Learning Modules | No. of Formulas |

|---|---|

| 3 | 0 |

Level 2 Ethics 2026 Syllabus, Readings, and Changes

| No. of Learning Modules – 3 | No. of LOS – 6 | |

|---|---|---|

Summary Dives deeper into CFAI Code of Ethics and Standards of Professional Conduct and how you can use these codes and standards to resolve ethical conflicts in the investment profession. You will confront numerous case applications. | ||

Code of Ethics and Standards of Professional Conduct

This reading dives deeper into the nuances of the Standards of Practice Handbook presented in the analog CFA Level 1 Ethics chapter. You will study the 6 components of the Code of Ethics and the 7 Standards of Professional Conduct.

Guidance for Standards I-VII

You must demonstrate their knowledge of the CFAI Code of Ethics and Standards of Professional Conduct through its application. The 7 standards were presented in a similar reading for Level 1. The reading recommends various procedures that you will use to prevent code and standard violations and best practices from upholding them.

Application of the Code and Standards: Level 2

Like the related reading in CFA Level 1 Ethics, this reading will show how to apply the CFAI Codes and Standards to various real-world situations. You will learn about the ethical decision-making process and readily identify where particular Codes and Standards are considered relevant.

CFA Ethics Level 2 Sample Questions and Answers

These sample questions here are typical of the L2 exam’s complexity and depth – formatted as item sets, with a vignette to deliver a scenario that tests the CFA L2 curriculum. On the actual exam, each vignette applies to 4 questions. We’ve provided a few extra questions for you to practice with. Be sure to review the illustrated answer explanations we’ve provided for each question. UWorld’s QBank is designed to expose you to exam-like questions and explain the concepts tested thoroughly.

What to Expect in CFA Level 3 Ethics?

CFA Level 3 Ethics is one of the most heavily weighted topics on the exam, with a weighting of 10-15%. The topic material reiterates and expands on content from the CFA Level 1 and Level 2 Ethics. However, there are two additional sections:

- Asset Manager Code of Professional Conduct

- Global Investment Performance Standards (GIPS)

Level 3 questions are mixed between “constructed response” (essay) and 44 item-set, multiple-choice questions. The exam tests the candidates’ ability to apply ethical frameworks to complex situations and explain the reasoning behind their conclusions.

Level 3 Ethics 2026 Syllabus, Readings, and Changes

The CFA Level 3 Ethics topic has a weighting of 10-15%. There could be a blend of item set questions (44 total) and constructed response (essay) questions.

Code of Ethics and Standards of Professional Conduct

At this point, candidates should be familiar with the Standards of Practice Handbook and how to apply its content to real ethical dilemmas faced by investment professionals on a daily basis. This reading will focus more on procedures for preventing Ethics violations and the application of concepts to more complex situations.

Guidance for Standards I–VII

Candidates must demonstrate their knowledge of the CFA Institute Code of Ethics and Standards of Professional Conduct through its application. The seven standards were presented in the “Guidance for Standards I–VII” section for Level 1.

Application of the Code and Standards: Level III

Like the related sections in CFA Level 1 and Level 2 Ethics, this reading will show how to apply the CFAI Codes and Standards to various real-world situations. Candidates will learn about the ethical decision-making process and readily identify where particular Codes and Standards are considered relevant.

Asset Manager Code of Professional Conduct

The CFA Institute Asset Manager Code enumerates the ethical responsibilities regarding asset management. The six categories are:

- Loyalty to clients

- Investment process and actions

- Trading

- Risk Management, compliance, and support

- Performance reporting and valuation

- Disclosures

Organizations typically have unique standards of conduct. The CFA Institute Asset Manager Code makes it easy for clients to identify which organizations follow a particular set of ethical principles. The reading introduces candidates to this code, how to follow it, and why it is important.

Overview of the Global Investment Performance Standards (GIPS)

Candidates will be familiar with GIPS from the related Level 1 reading. GIPS is a voluntary ethical guideline for reporting investment performance, designed by CFA Institute in partnership with GIPS Standards sponsors and industry experts. Investment firms and asset owners abide by GIPS as a pledge of ethical integrity and transparency to investors.

Candidates will learn more about the valuation hierarchy of the GIPS standards, the role of investment mandates and objectives, and the need for globally accepted standards for investment management firms.