What to Expect in CFA Level 1 Alternative Investments

This topic explores Alternative Investments, including hedge funds, private equity, real estate, commodities, and infrastructure. In this curriculum, CFAI defines Alternative Investments, their common characteristics, and their usefulness in creating diversification and higher returns.

Exam Weighting

The CFA Level I Alternative Investment weighs 7-10% of the total exam content, so approximately 13-18 CFA Level I exam questions focus on this topic.

| No. of Learning Modules | No. of Formulas |

|---|---|

| 7 | Nearly 15 |

Level 1 Alternative Investments 2026 Syllabus, Readings, and Changes

The CFA Level 1 exam includes 7 total learning modules for 2026. Numerous new texts have been added to the curriculum at all 3 levels, substantially expanding the focus on the topic area of Alternative Investments.

| No. of Learning Modules – 7 | No. of LOS – 22 | |

|---|---|---|

Summary This reading provides a comprehensive introduction to Alternative Investments. Alternative investments are asset classes or investment vehicles that supplement traditional long-only stocks, bonds, and cash positions. Alternative investments include 5 main categories: hedge funds, private capital, natural resources, real estate, and infrastructure. | ||

This significant change expands the discussion of alternatives and gives more information on how to use them in an investment strategy. In-depth exploration of alternative asset classes, risk management, and alternative investment structures are combined with fundamental knowledge to produce a simplified learning experience.

Alternative Investment Features, Methods, Structures, Performance, and Returns

This topic focuses on understanding the features and categories of alternative investments. It delves into the distinctions between direct investment, co-investment, and fund investment methods within alternative investments.

Additionally, the discussion explores prevalent investment ownership and compensation structures commonly employed in alternative investments.

Investments in Private Capital: Equity and Debt

Since they may be infrequently and/or privately traded, pricing, valuation, and performance can be much more difficult to assess for alternative investments. This learning module explores the factors, models, and circumstances that impact performance evaluation.

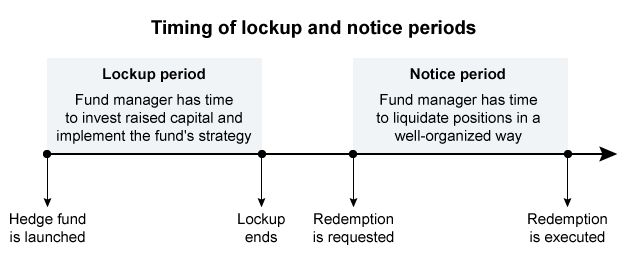

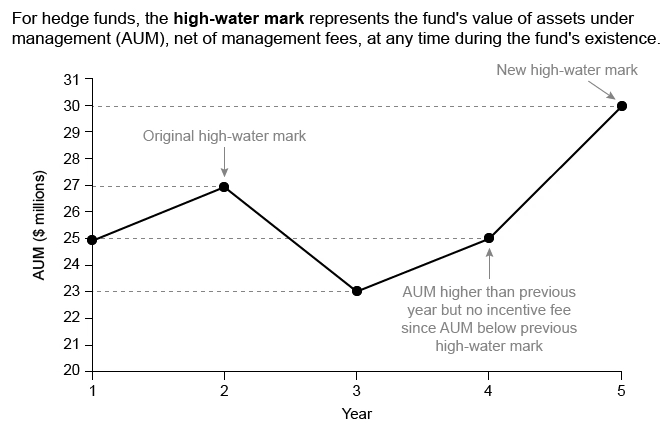

Private Capital, Real Estate, Infrastructure, Natural Resources, and Hedge Funds

This learning module looks at the various categories of alternative investments and their specific characteristics, risks, and returns.

Introduction to Digital Assets

This topic explores the financial applications of distributed ledger technology. It explains the investment features of digital assets and provides a comparative analysis with other asset classes. The discussion also covers various investment forms and vehicles utilized in digital asset investments. Additionally, it involves analyzing sources of risk, return, and diversification within the landscape of digital asset investments.

CFA Alternative Investments Level 1 Sample Questions and Answers

These sample questions are typical of the probing multiple-choice questions on the L1 exam. During the exam, you have about 90 seconds to read and answer each question, carefully designed to test knowledge from the CFA curriculum. UWorld’s question bank is built to expose you to exam-like questions and illustrate and explain the concepts tested thoroughly.

What to Expect in CFA Level 2 Alternative Investments

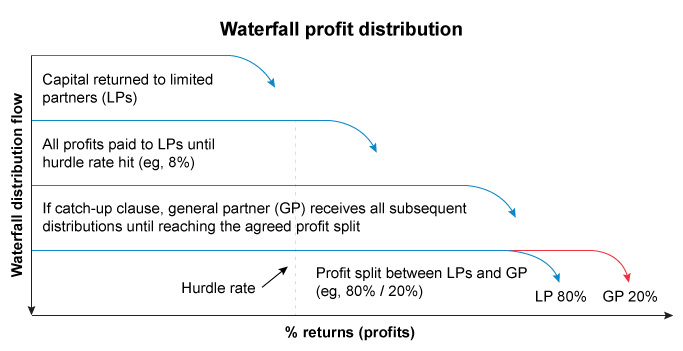

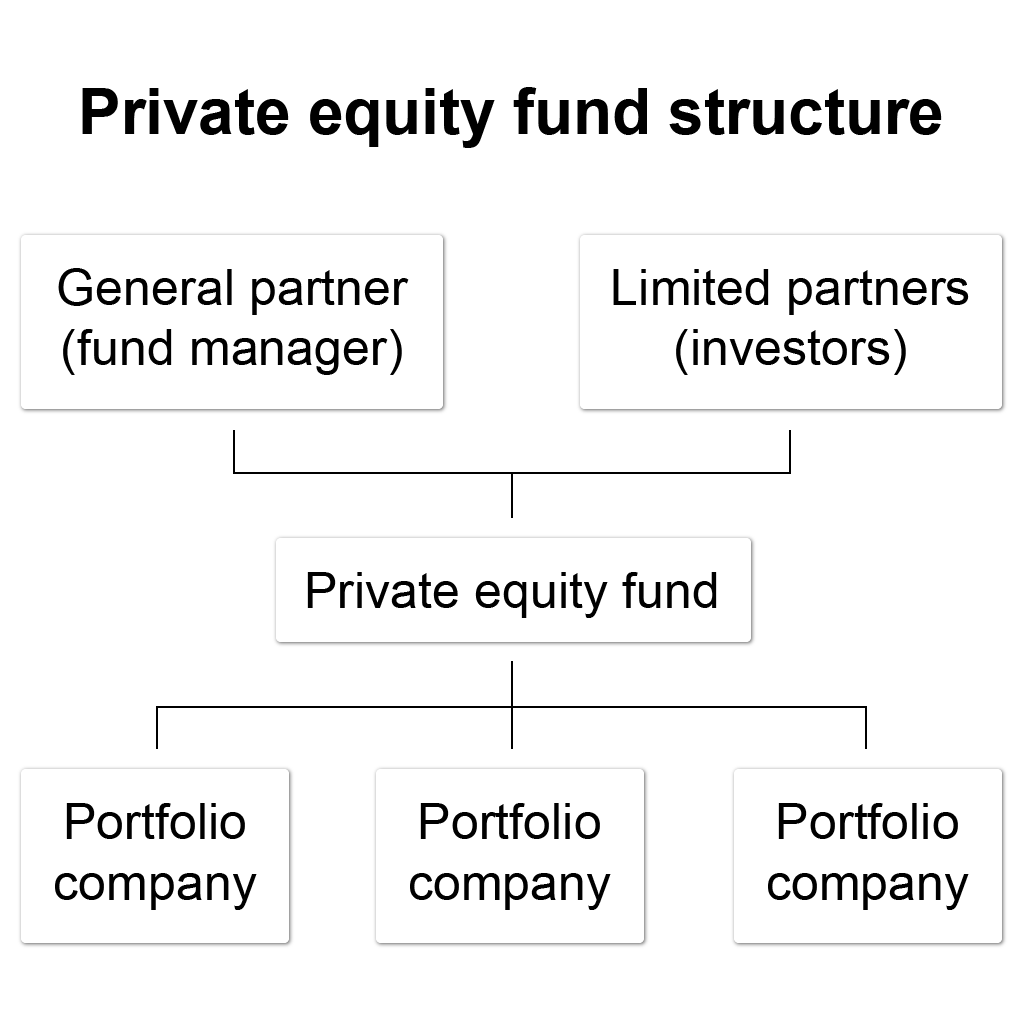

These readings focus on real estate, private equity, and commodities and describe real estate investments, both private and public, and methods for analysis and evaluation. Private equity, including venture capital and leveraged buyouts, is examined from the perspectives of a private equity firm evaluating equity portfolio investments and an investor considering participation in a private equity fund. Strategies involving commodity hedging are also discussed.

The CFA Level 2 Alternative Investment (AI) is fundamental to passing CFA Level 2 and succeeding in the CFA overall.

Exam Weighting

CFA Alternative Investment has a weighting of 5-10% of the total exam content, such that approximately 4-8 questions or 1-2 item sets focus on this topic.

| No. of Learning Modules | No. of Formulas |

|---|---|

| 4 | Around 20 |

Level 2 Alternative Investments 2026 Syllabus, Readings, and Changes

The 2026 CFA Level 2 exam comprises 4 learning modules. Notably, Private Equity Investments have been removed from the readings, and Hedge Fund Strategies have been introduced into the curriculum.

| No. of Learning Modules – 4 | No. of LOS – 29 | |

|---|---|---|

|

Summary

These learning modules focus on the following categories of Alternative Investments: real estate, private equity, and commodities. Real estate investments, both private and public, are described, and methods for analysis and evaluation are presented. Private equity, including venture capital and leveraged buyouts, is examined from the perspectives of a private equity firm evaluating equity portfolio investments and of an investor considering participation in a private equity fund. |

||

Although it is commonly known that real estate contributes significantly to a balanced portfolio’s diversification, you should be aware of how significantly the risk profile of real estate investments varies depending on the type of asset. The Real Estate Investments material describes the risk profile of real estate debt vs equity (as a lender or owner of mortgage-backed securities), primarily focusing on commercial real estate.

Overview of Types of Real Estate Investments

Real estate property holds substantial importance within investment portfolios, offering an appealing source of current income.

This learning module comprehensively compares the features, classifications, primary risks, and fundamental structures of public and private real estate investments. It also delves into real estate’s roles in portfolios and the factors determining its economic value.

The module also explores various commercial property types, shedding light on their unique investment traits. It covers the due diligence procedures applicable to both private and public equity real estate investments. Additionally, it addresses real estate investment indexes, including their construction methods and potential biases

Investments in Real Estate through Publicly Traded Securities

These learning modules compare various characteristics, classifications, and risks for public and private real estate investments. They also describe the valuation principles and approaches for pricing alternative assets and discuss the advantages and disadvantages of investing in real estate through publicly traded securities compared to private vehicles.

Introduction to Commodities and Commodity Derivatives

This reading discusses commodities and commodity futures, including scenarios of contango and backwardation for futures prices.

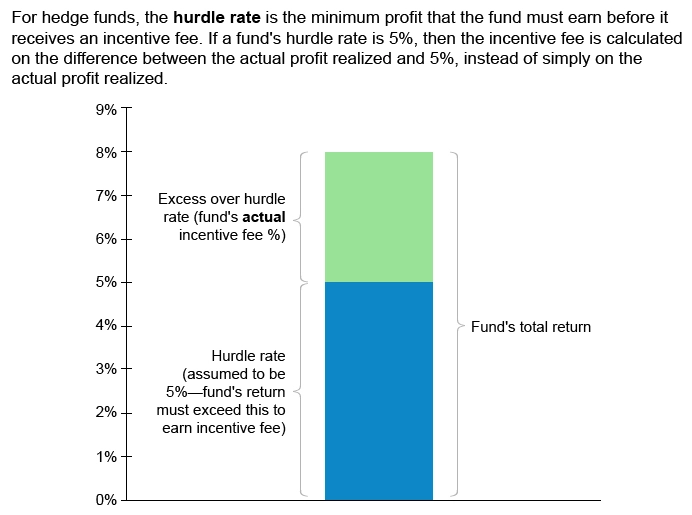

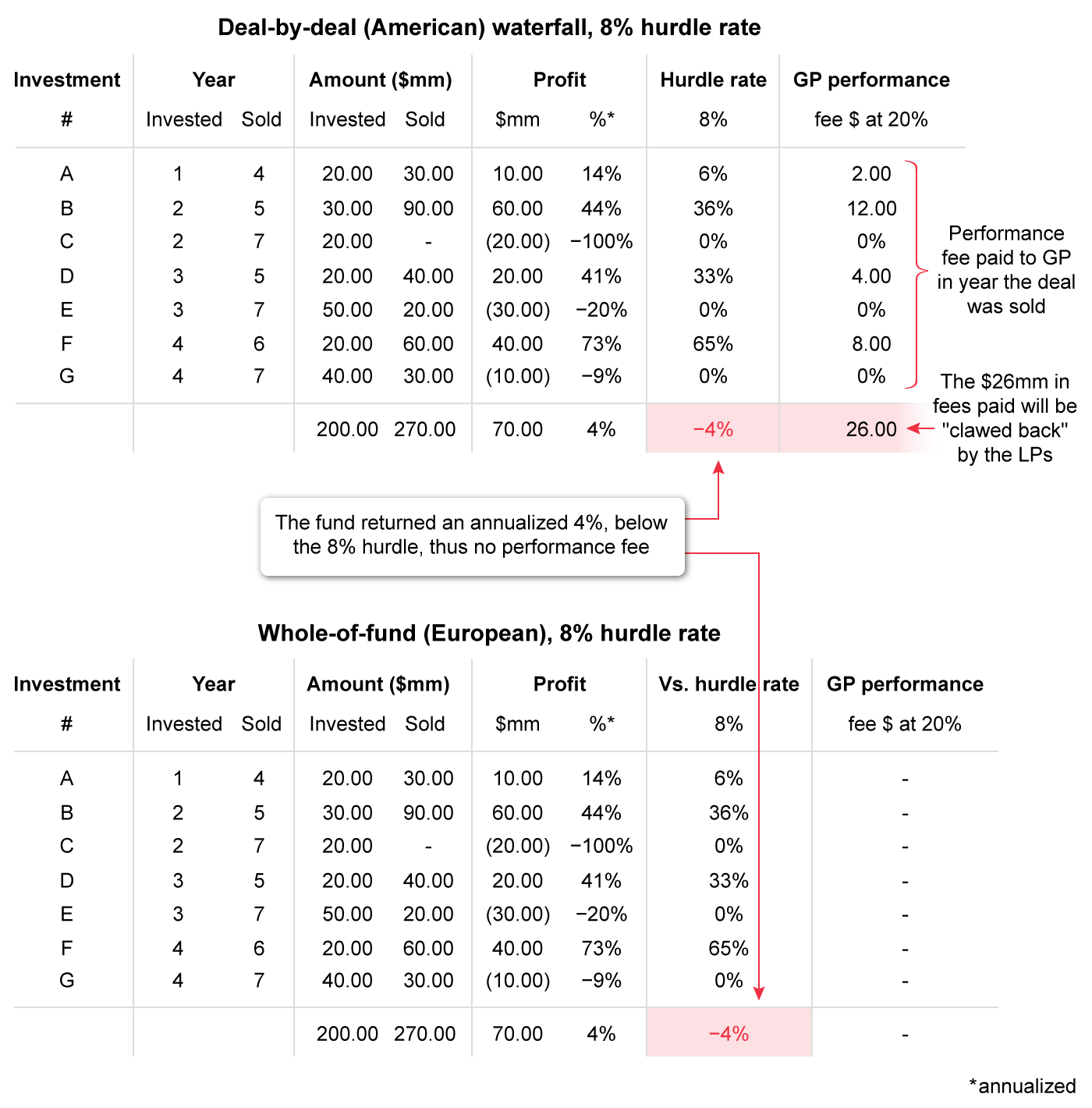

Hedge Fund Strategies

This topic classifies hedge fund strategies, including equity-related, event-driven, relative value, opportunistic, specialist, and multi-manager strategies. It delves into the investment characteristics, strategy implementation, and the role each plays in a portfolio. Additionally, the discussion encompasses how factor models can be utilized to comprehend hedge fund risk exposures and evaluate the impact of allocating to a hedge fund strategy within a traditional investment portfolio.

CFA Alternative Investments Level 2 Sample Questions and Answers

These sample questions exemplify the level of complexity and depth encountered in the Level 2 exam. They are presented as item sets, each accompanied by a vignette that creates a scenario designed to assess your understanding of the CFA Level 2 curriculum. It’s worth noting that each vignette applies to 4 questions on the actual exam, but we’ve included a few extra questions to enhance your learning experience. We strongly recommend reviewing the detailed answer explanations provided for each question. UWorld’s question bank will familiarize you with exam-style questions and provide comprehensive explanations to help you grasp the tested concepts thoroughly.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

What to Expect in CFA Level 3 Alternative Investments?

Alternative Investments does not appear as a separate topic area at Level 3. Instead, AI concepts including private equity, real estate, commodities, and hedge fund exposures are integrated into portfolio allocation, risk budgeting, and multi-asset strategies within Portfolio Management.