What to Expect in CFA Level 1 Fixed Income

On the CFA Institute’s Level 1 exam, Fixed Income is among the top 3 most heavily weighted topics, along with Financial Statement Analysis and Ethics.

You are taught to define fixed income securities and calculate and interpret their associated features. The material covers securitization, the fundamentals of credit risk, and the influence of interest rates on bond returns

Exam Weighting

The CFA Fixed Income topic has a weight of 11-14% of the total exam content, so that approximately 20-25 of the 180 CFA Level 1 exam questions focus on this topic.

| No. of Learning Modules | No. of Formulas |

|---|---|

| 19 | ca. 40 |

Level 1 Fixed Income 2026 Syllabus, Readings, and Changes

TheCFA Level 1 curriculum has about 19 readings for Fixed Income (8.2% of the total curriculum).

| No. of Learning Modules – 19 | No. of LOS – 51 | |

|---|---|---|

|

Summary

The learning modules introduce attributes of various Fixed Income securities and how to calculate and interpret bond prices, yields, and spreads, and then also introduces securitization and provides an overview of global debt markets. The material covers fundamentals of bond returns and risks with special attention given to interest rates and credit risk. It also introduces key factors for assessing bond sensitivity and credit analysis.

|

||

Fixed-Income Instrument Features

The focus of the topic is on understanding fixed-income instruments, encompassing the description of their features. Additionally, you are expected to delve into the contents of a bond indenture, emphasizing the ability to contrast affirmative and negative covenants.

Fixed Income Markets: Issuance and Trading

Global Fixed Income markets include publicly traded securities and non-publicly traded loans. These markets typically attract less attention despite being 3 times larger than global equity markets.

The learning module presents a summary of global fixed income markets and their major players. You will be introduced to fixed income indexes and fixed income trading in secondary markets.

Fixed-Income Cash Flows and Types

This topic focuses on comprehending fixed-income cash flows and types. This involves describing the common cash flow structures of fixed-income instruments and contrasting cash flow contingency provisions that benefit issuers and investors. Additionally, you are expected to articulate how legal, regulatory, and tax considerations impact the issuance and trading of fixed-income securities.

Fixed-Income Markets for Corporate Issuers

Many kinds of assets generate cash flows for their investors, such as mortgages, auto loans, student loans, bank loans, etc. When those cash flows are securitized, they pass through an entity that repackages them as fixed income securities, and their cash flows become the basis of that asset’s value. Special entities issue these securities as asset-backed securities (ABS).

You will be introduced to the benefits of securitization for investors, issuers, economies, and financial markets. The learning module also explores the various characteristics of different ABS types and their associated risks.

Fixed-Income Markets for Government Issuers

The focus of this topic is on understanding funding choices made by sovereign and non-sovereign governments, quasi-government entities, and supranational agencies. You are expected to describe these funding choices. The topic also involves contrasting the issuance and trading of government and corporate fixed-income instruments.

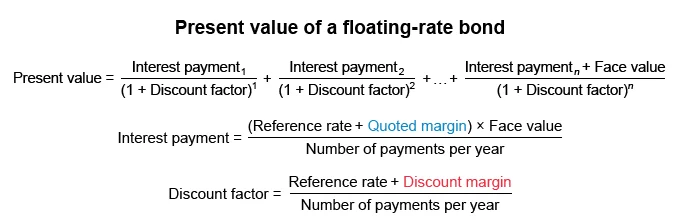

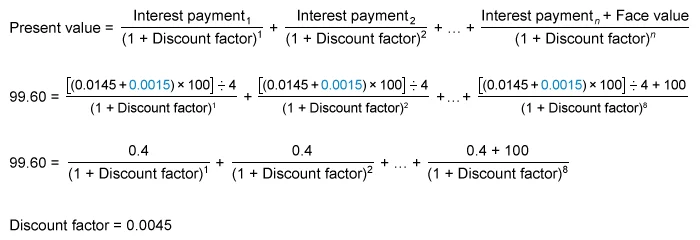

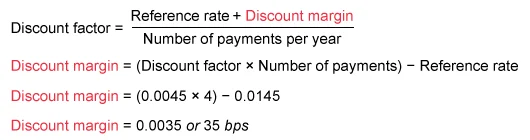

Yield and Yield Spread Measures: Fixed Rate Bonds and Floating Rate Instruments

The focus of this section is on the ability to calculate the annual yield on a bond for varying compounding periods within a year. Additionally, you are expected to compare, calculate, and interpret yield and yield spread measures for fixed-rate bonds. Similarly, in the context of yield and yield spread measures for floating-rate instruments, the emphasis is on the capability to calculate and interpret yield spread measures for such instruments and calculate and interpret yield measures specifically tailored for money market instruments.

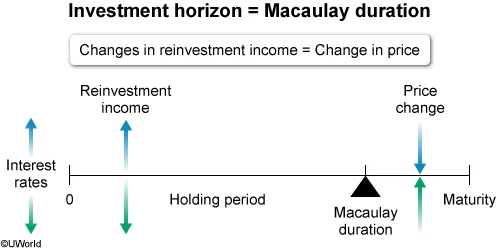

Fixed-Income Risk and Credit Analysis (An Overview)

This section covers essential concepts in fixed-income risk and credit analysis:

| Yield-Based Bond Measures |

|

| Yield-Based Bond Convexity and Portfolio |

|

| Curve-Based and Empirical Risk Measures |

|

| Credit Risk |

|

| Credit Analysis for Government and Corporate Issuers |

|

| Fixed-Income Securitization |

|

CFA Fixed Income Level 1 Sample Questions and Answers

These sample questions are typical of the probing multiple-choice questions on the CFA L1 exam. During the exam, you have about 90 seconds to read and answer each question, carefully designed to test knowledge from the CFA curriculum. UWorld’s question bank is built to expose you to exam-like questions and illustrate and explain the concepts tested thoroughly.

What to Expect in CFA Level 2 Fixed Income

The CFA Level 2 Fixed Income is one of the most heavily weighted topics on the exam. The material introduces traditional and modern theories regarding the shape of the yield curve and the fundamental relationships underpinning its composition. You will study valuation methods used to value bonds with embedded options and various credit analysis concepts.

Exam Weight

The CFA Fixed Income topic has a weight of 10-15% of the total exam content, so that approximately 8-12 questions or 2-3 item sets on the CFA Level 2 exam focus on this topic.

| No. of Readings | No. of Formulas |

|---|---|

| 5 | ca. 60 |

Level 2 Fixed Income Syllabus, Readings, and Changes

The CFA Level 2 curriculum includes 5 learning modules for the Fixed Income topic (10% of the total curriculum). There have been only minor updates to the L2 Fixed Income curriculum.

| No. of Learning Modules – 5 | No. of LOS – 50 | |

|---|---|---|

Summary These learning modules focus on the following categories of Alternative Investments: real estate, private equity, and commodities. The Fixed Income curriculum introduces the yield curve and fundamental aspects of its composition. You will learn various theories regarding yield curve shape and an arbitrage-free framework for valuing option-free bonds. It then builds on binomial valuation methods to value bonds with embedded options. You will study credit analysis, the term structure of credit spreads, and how credit default swaps are used in managing credit exposure. | ||

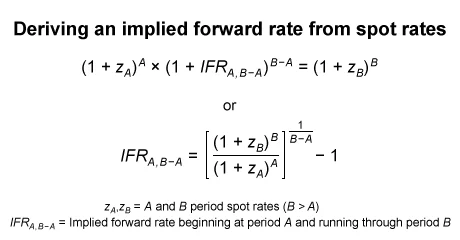

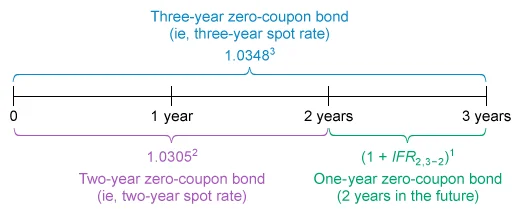

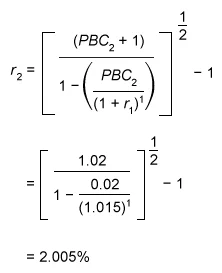

The Term Structure and Interest Rate Dynamics

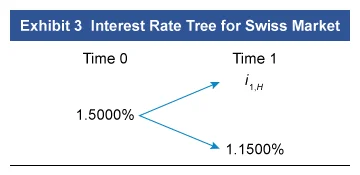

Interest rates act to influence and measure the economy. Quantifying interest rate risk is an important skill for risk managers, and understanding the determinants of interest rates is important for issuers of and investors in fixed-income securities.

The learning module explains spot rates and forward rates and their influence on the yield curve shape. You will build on this information to understand how forward rates influence the yield-to-maturity and expected bond returns.

The Arbitrage-Free Valuation Framework

Valuing fixed income securities, derivatives, and other financial assets is predicated on the idea that market prices adjust until arbitrage opportunities expire

The learning module introduces concepts and techniques for no-arbitrage valuation of Fixed Income securities. This includes discussions of the binomial interest rate tree and a Monte Carlo forward-rate simulation.

Valuation and Analysis of Bonds with Embedded Options

The value of embedded options is typically contingent on interest rates. This makes bond valuation more complex when a bond has one or more embedded options. Bond issuers and investors must understand how various embedded options influence bond values and their sensitivity to interest rate changes.

The learning module introduces a summary of different types of embedded options before exploring bonds that include a call or put provision. You will also learn about how option-adjusted spreads are used to value risky callable and putable bonds.

Credit Analysis Models

Credit analysis models rely on inputs such as exposure to default loss, the loss given default, and the probability of default. These models are an important part of valuing corporate and government bonds.

You are introduced to structural and reduced-form credit analysis models. The learning module also covers the arbitrage-free framework and compares the credit analysis for securitized debt with that of corporate bonds.

Credit Default Swaps

A credit default swap is a financial contract between 2 parties that enables an investor to “swap” or offset credit risk with another investor for a defined period of time. These derivative instruments are broadly used internationally.

The learning module classifies these instruments and explores their fundamental concepts. You will learn about the elements associated with their valuation, pricing, and applications.

CFA Fixed Income Level 2 Sample Questions and Answers

These sample questions are typical of the L2 exam’s complexity and depth – formatted as item sets, with a vignette to deliver a scenario that tests the CFA L2 curriculum. On the actual exam, each vignette applies to 4 questions. We’ve added a few additional questions for you to practice with. Be sure to review the illustrated explanations we’ve provided for each question. UWorld’s question bank is designed to expose you to exam-like questions and explain the concepts tested thoroughly.

{kind=link}

{kind=link}

{kind=link}

What to Expect in CFA Level 3 Fixed Income?

Fixed Income is no longer a stand-alone topic at Level 3, but it is heavily integrated into Portfolio Management. Bond valuation concepts, yield curve dynamics, interest rate risk, and liability-driven investing all reappear inside PM and Wealth Management readings.