What to Expect in CFA® Level 1 Derivative Investments

The Derivative Investments curriculum has a similar weighting to that of alternative investments and portfolio management. There are 10 Level 1 learning modules dedicated to the topic. You will study various derivative instruments classified as forward commitments and contingent claims and see how they derive their value and are traded in different settings.

Exam Weighting

The CFA Level 1 Derivative Investments has a weighting of 5-8% which implies that around 9-14 out of 180 CFA Level 1 exam questions focus on this topic.

| No. of Learning Modules | No. of Formulas |

|---|---|

| 10 | Around 12 |

Level 1 Derivative Investments 2026 Syllabus, Readings, & Changes

There are 10 learning modules for CFA Level I DI in 2026. These learning modules begin with an overview of derivative instruments and markets, distinguishing characteristics of forward commitments and contingent claims, and the derivative’s relation to the underlying asset. They then cover the purpose, benefits, and risks of Derivative Investments, as well as criticisms and potential misuse.

The material remains essentially unchanged, with minor updates. The following table provides a brief description of the topic curriculum:

| No. of Learning Modules – 11 | No. of LOS – 22 | |

|---|---|---|

Summary This paper discusses the fundamentals of derivative instruments, including forward commitments (e.g., futures, forwards, swaps) and contingent claims (e.g., call and put options), and derivative markets such as exchange-traded and over-the-counter derivative markets. It further explains derivative pricing and valuation and introduces the principle of arbitrage. | ||

Derivative Instrument and Derivative Market Features

The reading focuses on defining derivatives and elucidates the basic features of derivative instruments. It also provides insights into the characteristics of derivative markets, distinguishing between over-the-counter and exchange-traded markets.

Forward Commitment and Contingent Claim Features and Instruments

This reading emphasizes defining various derivative instruments such as forward contracts, futures contracts, swaps, options (calls and puts), and credit derivatives. It also involves comparing their essential characteristics and understanding the value and profit determination for call-and-put options.

Derivative Benefits, Risks, and Issuer and Investor Uses

The focus here is on describing the benefits and risks associated with derivative instruments. Additionally, it compares how derivatives are utilized among issuers and investors.

Arbitrage, Replication, and the Cost of Carry in Pricing Derivatives

This reading centers on explaining the concepts of arbitrage and replication in pricing derivatives. It also differentiates between the spot and expected future prices of an underlying asset and the cost of carry associated with holding the underlying.

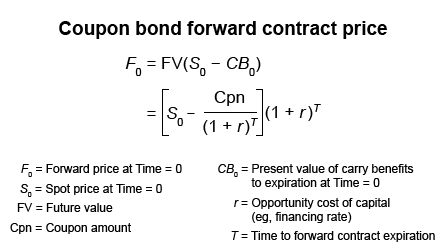

Pricing and Valuation of Forward Contracts and for an Underlying with Varying Maturities

The primary focus of this reading is to explain the determination of the value and price of a forward contract throughout its life. It also covers the determination of forward rates for interest rate forward contracts and their applications.

Pricing and Valuation of Futures Contracts

Here, the reading aims to compare the value and price of forward and futures contracts while explaining the reasons for the differences in forward and futures prices.

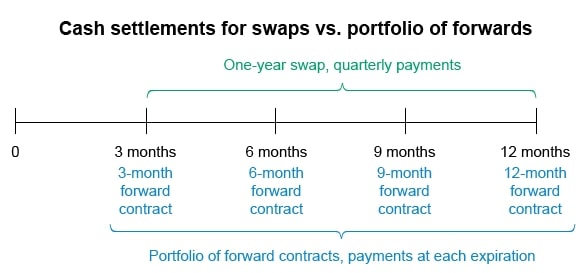

Pricing and Valuation of Interest Rates and Other Swaps

This reading delves into how swap contracts are similar to, yet different from, a series of forward contracts. It also contrasts the value and price of swaps.

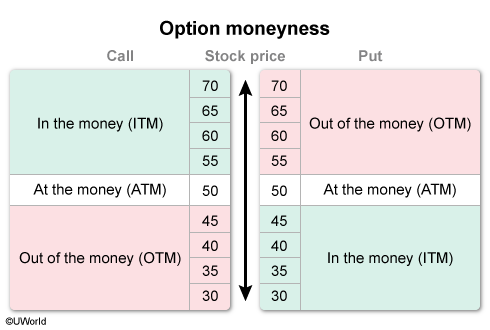

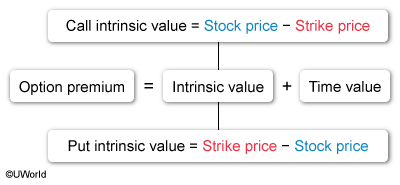

Pricing and Valuation of Options

This reading’s primary focus is to explain an option’s exercise value, moneyness, and time value. It also contrasts the use of arbitrage and replication concepts in pricing forward commitments and contingent claims, identifying factors influencing option value.

Option Replication Using Put–Call Parity

In this reading, the emphasis is on explaining put–call parity for European options and put-call-forward parity for European options.

Valuing a Derivative Using a One-Period Binomial Model

This reading revolves around explaining how to value a derivative using a 1-period binomial model and describing the concept of risk neutrality in derivatives pricing.

CFA Derivative Investments Level 1 Sample Questions and Answers

These sample questions are typical of the probing multiple-choice questions on the L1 exam. During the exam, you have about 90 seconds to read and answer each question, carefully designed to test knowledge from the CFA curriculum. UWorld’s question bank is built to expose you to exam-like questions and illustrate and explain the concepts tested thoroughly.

What to Expect in CFA Level 2 Derivative Investments

The CFA Level 2 Derivative Investments curriculum picks up where the Level 1 curriculum left off and further explores derivatives instruments and markets. It includes some of the curriculum’s more detailed and “mathy” portions as it dives into derivative pricing and valuation. It is often some of the least familiar material for applicants, making it more challenging to master.

Exam Weighting

The CFA Level 2 Derivative Investments topic has an exam weight of 5-10%, implying that around 4-8 questions or 1-2 item sets will focus on this topic.

| No. of Readings | No. of Formulas |

|---|---|

| 2 | Around 20 |

Level 2 Derivative Investments 2026 Syllabus, Readings, and Changes

The 2026 CFA Level 2 curriculum covers Derivative Investments across 2 learning modules. It’s important to highlight that there are no substantial changes in the Derivative Investments curriculum for CFA Level 2.

| No. of Readings – 2 | No. of LOS – 21 | |

|---|---|---|

Summary Introduces key pricing and valuation concepts of forward commitments, including forwards, futures, and swaps as well as valuation of contingent claims, that is, options. “Greeks,” which measure the effects on the value of small changes in underlying asset value, time, volatility, and the risk-free rate, are also discussed. | ||

Pricing and Valuation of Forward Commitments

The Pricing and Valuation of Forward Commitments learning module offers comprehensive insights into the pricing and valuation of forwards, futures, and swaps. It enhances your understanding by incorporating clear and easily digestible images and graphics.

The module covers the pricing and valuation of futures using various approaches, including the arbitrage-free method and offsetting bond portfolios. This content is particularly valuable for specialists relying on forwards and swaps to manage a wide array of market risks.

This knowledge is especially relevant for professionals such as private wealth managers, who employ futures to hedge their clients’ equity risk; pension scheme managers, who use swaps to mitigate interest rate risk; or university endowment managers, who utilize Derivative Investments for tactical asset allocation and portfolio rebalancing. The module can be customized to cater to the specific needs of these professionals.

Valuation of Contingent Claims

This reading centers on the binomial option valuation model, emphasizing the capacity to articulate and decipher its constituent elements. You will gain the ability to assess the worth of European options by factoring in the present value of anticipated payouts upon maturity. The material encompasses the identification of arbitrage opportunities, the computation of no-arbitrage values through a 2-period binomial model, and the interpretation of interest rate option values. It also delves into the assumptions and practical use of the Black-Scholes-Merton model in appraising a variety of options. Mastery of option Greeks, the execution of a delta hedge, the grasp of gamma risk, and the definition of implied volatility constitute the fundamental components of this succinct study.

CFA Derivative Investments Level 2 Sample Questions and Answers

These sample questions are typical of the L2 exam’s complexity and depth – formatted as item sets, with a vignette to deliver a scenario that tests the CFA L2 Curriculum. (On the actual exam, each vignette applies to 4 questions; we’ve provided a couple extra so you can practice thoroughly). Be sure to review the illustrated explanations we’ve provided for each question. UWorld’s question bank is designed to expose you to exam-like questions and explain the concepts tested thoroughly.

{kind=link}

{kind=link}

What to Expect in CFA Level 3 Derivative Investments?

Derivatives is not a stand-alone topic in Level 3, but derivatives concepts such as options, futures, swaps, and hedging techniques are embedded in portfolio construction, risk management, and currency management readings.